2026 AI Investment Outlook: Where Smart Money Is Heading Next

As 2025's AI spending approaches $2 trillion and venture capital pours $193 billion into the sector, institutional investors are shifting from hyperscalers to specialized AI subsectors. Edge computing, agentic AI, cybersecurity, and infrastructure stocks offer better risk-reward ratios for 2026 as the market matures beyond the early AI boom.

2026 AI Investment Outlook: Where Smart Money Is Heading Next

As November winds down and institutional investors finalize their 2026 portfolios, a profound shift is underway in artificial intelligence investing. After three years of explosive growth concentrated in a handful of hyperscalers—Nvidia, Microsoft, Google, Meta, and Amazon—smart money is now hunting for opportunities beyond the obvious winners. The numbers tell a compelling story: Global AI spending is projected to hit $2 trillion by year-end 2026, with venture capital investments reaching $193 billion in just the first three quarters of 2025.[1][2] Yet beneath these staggering figures lies a more nuanced reality: The AI investment landscape is fracturing into specialized subsectors, each with distinct risk profiles, growth trajectories, and return potential.

For investors who rode the first wave of AI enthusiasm—watching Nvidia surge 700% since ChatGPT's launch and the "Magnificent Seven" tech giants dominate S&P 500 returns—2026 represents a pivotal moment.[3] The easy gains from betting on AI infrastructure leaders may be behind us, as valuations stretch to extremes and questions about return on investment grow louder. Goldman Sachs analysts recently warned that while AI could boost global productivity by 1% annually, current spending levels may outpace near-term revenue generation, creating a "valley of disappointment" for investors expecting immediate returns.[4]

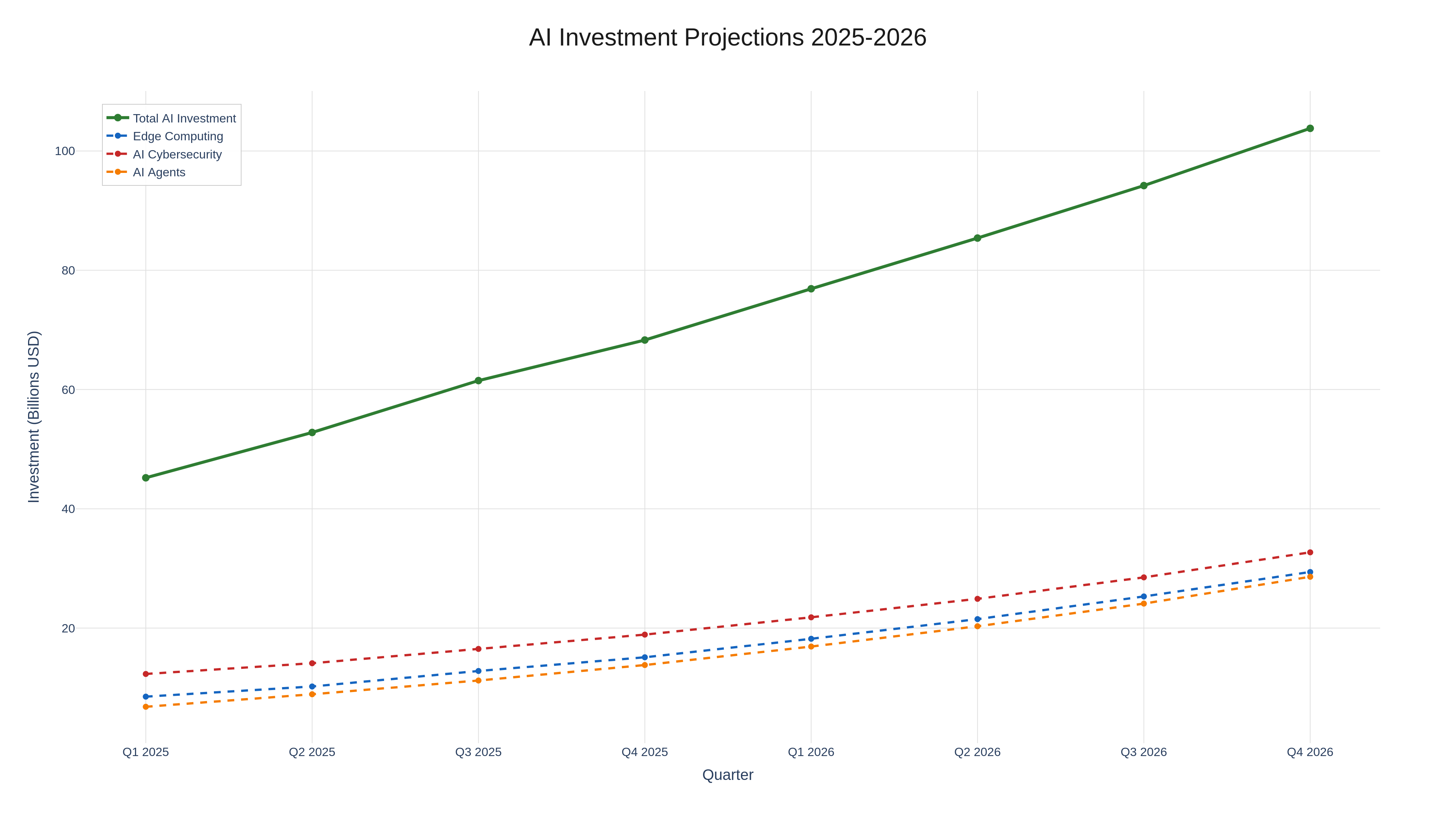

AI investment projections show robust growth across edge computing, cybersecurity, and AI agents subsectors through 2026

Yet opportunity abounds for those willing to look beyond the headlines. Edge computing is projected to surpass $50 billion by 2026 as AI workloads move closer to data sources.[5] Agentic AI—autonomous systems capable of independent decision-making—is experiencing 300% year-over-year funding growth and could capture $10.5 billion in market value by 2026.[6] AI cybersecurity investments are accelerating at 22% annually as organizations race to defend against AI-powered threats.[7] And venture capital, despite a 40% decline in deal volume, is concentrating capital in proven AI business models with clear paths to profitability.[8]

This article provides a comprehensive roadmap for navigating AI investments in 2026. We analyze four high-potential subsectors backed by institutional money, examine venture capital trends reshaping the funding landscape, evaluate ROI expectations as enterprises demand measurable returns, and offer strategic frameworks for balancing risk and reward in a maturing AI market.

The Great Rebalancing: Why 2026 Marks an AI Investment Inflection Point

From Hype to ROI: The Market's New Discipline

The exuberance that characterized AI investing in 2023 and 2024 is giving way to a more measured approach in 2026. Forrester Research predicts that many enterprises will delay up to 25% of planned AI spending until 2027 as they struggle to demonstrate tangible returns, with only 15% of AI decision-makers reporting earnings increases over the past year.[9] This "Great AI Reality Check," as SAS analysts call it, represents a necessary market correction where accountability replaces unchecked innovation.[10]

CFO sentiment reflects this shift dramatically. PYMNTS Intelligence data shows that just 26.7% of chief financial officers expect to increase AI budgets in the next 12 months—down from 53.3% a year earlier—as ROI becomes the primary filter for investments.[11] Technology companies that led AI spending are maintaining investment levels, but other sectors are pulling back: Only firms reporting "very positive" AI returns are committing to budget increases, while those with negative ROI are reducing allocations by double digits.[12]

Yet this discipline is creating opportunities rather than eliminating them. Gartner's 2026 CIO Survey reveals that 89% of global chief information officers plan to increase AI spending, but with a critical difference: They're focusing on "agentic AI ROI" from production deployments rather than experimental pilots.[13] This represents a 35% year-over-year growth in a constrained budget environment, indicating that enterprises are reallocating resources from failed experiments toward proven use cases. The winners in 2026 will be companies and subsectors that can demonstrate measurable productivity gains, cost savings, or revenue growth—not just impressive technology demonstrations.

Concentration Risk and the Search for Diversification

The current AI investment landscape presents a concentration problem that sophisticated investors are actively addressing. AI infrastructure spending now accounts for 92% of U.S. GDP growth in early 2025, while non-AI sectors have stagnated.[14] Nvidia alone has contributed a disproportionate share of S&P 500 gains since 2022, creating what economists call the "Nvidia-state"—an economy overly dependent on a handful of AI companies.[15] This concentration is unsustainable and creates systemic risk.

Institutional investors are responding by seeking diversification across AI subsectors. UBS analysts note that while Microsoft Azure maintains 40% growth rates in AI cloud services and is projected to grow 28% annually through 2026, investors are increasingly worried about saturation in hyperscaler markets.[16] The solution? Allocate capital to specialized plays in edge computing, vertical-specific AI applications, autonomous systems, and infrastructure components beyond chips—areas where growth potential remains high but competition is less concentrated.

Venture capital firms are leading this rebalancing. In 2025's first half, generative AI captured $49.2 billion in funding (exceeding 2024's full-year total), but investments are shifting toward companies with defensible business models and sector-specific applications rather than horizontal AI platforms.[17] Foley & Lardner predicts a significant shakeout among horizontal AI startups lacking vertical specialization, with funding concentrating on companies demonstrating product-market fit and regulatory durability.[18] By 2026, the winners will likely be specialized AI applications in healthcare, finance, manufacturing, and other domains where AI solves specific, high-value problems.

Four AI Subsectors Where Smart Money Is Heading

1. Edge Computing and Distributed AI Infrastructure

Edge computing represents one of the most compelling AI investment opportunities for 2026, driven by the fundamental need to process data closer to its source rather than shuttling everything to centralized cloud data centers. The market is projected to exceed $50 billion by 2026, growing at a 36.9% compound annual growth rate, with AI integration serving as the primary catalyst.[19]

The investment thesis is straightforward: As AI applications proliferate in autonomous vehicles, IoT devices, smart cities, and industrial automation, latency requirements make centralized processing impractical. A self-driving car can't wait 100 milliseconds for a cloud server to process sensor data and return a steering decision. Medical diagnostic tools need real-time AI inference at the point of care. Manufacturing robots require instantaneous anomaly detection to prevent defects. These applications demand edge AI—and the infrastructure market is booming to meet this need.

Edge computing infrastructure represents a $50+ billion market opportunity as AI workloads shift closer to data sources

Edge computing infrastructure represents a $50+ billion market opportunity as AI workloads shift closer to data sources

Investment opportunities in edge computing span multiple categories:

Hardware and Semiconductors: Companies developing AI chips optimized for edge deployment—low-power processors, neural processing units, and application-specific integrated circuits—are experiencing 40% surges in patent filings and funding.[20] Intel and AMD are positioning inference-focused accelerators to compete with Nvidia's training-dominant chips, targeting the edge market where different performance characteristics matter. TSMC and other semiconductor foundries are expanding capacity for advanced nodes (3nm and below) that enable power-efficient edge AI chips.

Edge Software and Platforms: Software companies providing tools for deploying, managing, and updating AI models at scale across distributed edge devices represent another high-growth segment. The challenge isn't just running AI at the edge—it's orchestrating thousands or millions of edge nodes, managing model versions, monitoring performance, and ensuring security. Companies solving these operational challenges are attracting significant venture capital, with deal sizes averaging $100-300 million for late-stage rounds.[21]

5G and Connectivity Infrastructure: Edge computing's growth is tightly coupled with 5G network expansion, which provides the low-latency, high-bandwidth connectivity edge AI requires. Telecommunications equipment providers and network operators investing in edge computing capabilities are positioned to benefit from this convergence. Grand View Research notes that 5G integration is a primary driver of edge AI adoption, particularly in Asia-Pacific markets where infrastructure buildout is accelerating.[22]

Vertical-Specific Edge Solutions: The highest returns may come from companies applying edge AI to specific industries. Autonomous vehicle systems, healthcare diagnostics, retail analytics, and industrial IoT represent massive addressable markets where edge computing isn't optional—it's foundational. Source 1 highlights that by 2029, edge AI initiatives will exceed 50% of all AI deployments, driven by these vertical applications.[23]

Regional dynamics also matter. North America leads with 37.7% market share, but Asia-Pacific is the fastest-growing region, fueled by China and India's smart city initiatives and IoT expansion.[24] Investors with exposure to Asian edge computing companies may capture disproportionate growth as these markets leapfrog traditional infrastructure.

2. Agentic AI: Autonomous Systems and AI Agents

Agentic AI—systems capable of autonomous decision-making and task execution without constant human supervision—is emerging as the highest-growth AI subsector for 2026, with projections indicating the market will reach $10.5 billion (up from $5.4 billion in 2024) at a staggering 45.8% compound annual growth rate.[25]

The investment opportunity stems from AI's evolution from passive tools to active agents. Early AI applications required human prompts for every task: You asked ChatGPT a question, it answered. Next-generation agentic AI operates differently: You assign a goal ("optimize our supply chain to reduce costs by 15%"), and the AI agent autonomously gathers data, analyzes options, makes decisions, and implements changes—checking back with humans only for approval at critical junctures. This shift from reactive to proactive AI fundamentally expands the technology's value proposition.

Adoption statistics support aggressive growth projections. Pragmatic Coders reports that 88% of senior executives plan to increase AI budgets due to agentic AI, and 79% have already adopted it for productivity gains.[26] Gartner forecasts that by 2026, 40% of enterprise applications will incorporate task-specific AI agents, potentially generating 30% of enterprise software revenue by 2035 in a best-case scenario.[27] McKinsey data shows AI agents improving operational efficiency by 40% in IT and customer service sectors, with 15-50% of business processes potentially automated by 2027.[28]

Investment opportunities in agentic AI cluster around several categories:

Customer Service and Support: AI agents handling customer inquiries, troubleshooting, and issue resolution represent the most mature agentic AI market. Companies like Moveworks and Frame AI are deploying agents that resolve 80% of common customer service issues autonomously by 2029, according to Gartner projections.[29] This subsector is particularly attractive because ROI is immediate and measurable—reduced call center costs, faster resolution times, and improved customer satisfaction scores.

Enterprise Workflow Automation: Agentic AI platforms that automate knowledge work—legal document review, financial analysis, HR onboarding, procurement processes—are attracting massive venture capital. BCG estimates a 45% CAGR for this segment over the next five years, driven by enterprises seeking to augment (not replace) human workers with AI agents that handle routine tasks.[30] The market opportunity is enormous: McKinsey estimates that 20-40% of knowledge worker time is spent on tasks that AI agents could automate.

AI-Powered Robotics: Physical embodiment of AI agents through robotics is experiencing a renaissance, particularly in Europe where over $1 billion was invested in 2025.[31] General-purpose robots enabled by AI—capable of learning new tasks through demonstration rather than programming—represent a potential paradigm shift. Companies focusing on robot fleet software, embodied AI training, and data collection for physical tasks are attracting attention from both venture capital and corporate investors.

Agentic AI Infrastructure: The "picks and shovels" play in agentic AI involves companies providing the underlying platforms, orchestration tools, and guardrails that make autonomous agents safe and reliable. As Atera predicts, by 2026, 40% of CIOs will demand "guardian agents" for oversight, creating opportunities for companies building AI governance and monitoring solutions.[32]

Challenges remain significant. Trust and security issues top executive concerns, with 28% citing lack of trust as a barrier and 37% worried about security risks like data breaches and AI hallucinations.[33] Integration complexities and high implementation costs also restrain adoption, with 95% of IT leaders reporting hurdles.[34] Successful investments will target companies with robust governance frameworks, transparent AI operations, and proven security models—not just impressive technical demonstrations.

3. AI Cybersecurity: Defense in the Age of AI-Powered Threats

AI cybersecurity represents a paradoxical investment opportunity: AI is simultaneously the greatest threat and the most promising defense in modern cybersecurity. The market is projected to reach $93 billion by 2030 (implying approximately $45-50 billion by 2026) at a 21.9% CAGR, driven by the dual pressures of AI-enabled attacks and AI-powered defenses.[35]

The investment thesis centers on an escalating cyber arms race. Threat actors are already deploying AI to create adaptive malware, hyper-realistic phishing campaigns using voice cloning, and prompt injection attacks targeting AI systems themselves.[36] Google's 2026 Cybersecurity Forecast warns that AI will "supercharge cybercrime," necessitating corresponding investments in AI-driven defense capabilities.[37] This creates an imperative: Organizations have no choice but to adopt AI cybersecurity tools, making this subsector relatively recession-resistant.

AI cybersecurity investments are growing at 22% annually as organizations defend against AI-powered threats

AI cybersecurity investments are growing at 22% annually as organizations defend against AI-powered threats

Budget allocations confirm this priority. PwC's Global Digital Trust Insights survey reveals that 78% of organizations expect cyber budget increases in the coming year, with AI emerging as the top investment area for 36% of respondents—surpassing cloud security and data protection.[38] AI/ML tool usage has surged 594.82% from April 2023 to January 2024, indicating rapid integration, and 82% of IT decision-makers plan to allocate funds to AI-driven security solutions within the next two years.[39]

Investment opportunities in AI cybersecurity include:

Threat Detection and Response: AI-enabled threat hunting platforms that identify anomalies, predict attacks, and orchestrate automated responses represent the largest market segment. Source 3 reports that 48% of security leaders prioritize AI-driven threat hunting for faster detection and response, with applications in behavioral analysis, phishing detection, and incident forensics becoming standard by 2026.[40] Companies offering Security Operations Center (SOC) automation—where AI handles data correlation and initial response—are particularly attractive, as they address the chronic cybersecurity talent shortage.

Zero-Trust and Identity Security: As AI agents proliferate, managing their digital identities becomes a security imperative. Google predicts that "identity debt" and AI fragmentation—uncoordinated AI deployments creating new risks—will drive investments in platforms that monitor AI agents as distinct digital entities and enforce zero-trust security models.[41] This represents a greenfield opportunity as enterprises struggle to adapt security frameworks designed for human users to agentic AI.

AI Security Platforms (AISPs): A new category of tools focused specifically on securing AI systems themselves is emerging. These platforms detect adversarial attacks on AI models, monitor for data poisoning, prevent prompt injection exploits, and ensure AI governance compliance. With 77% of organizations feeling unprepared for AI-powered threats, AISPs could see explosive growth.[42]

Managed Security Services: Managed Service Providers (MSPs) integrating AI into cybersecurity offerings are experiencing strong demand, particularly from small and medium enterprises that lack in-house AI expertise. MSPs using AI to automate threat monitoring, vulnerability management, and incident response are positioned to capture market share as businesses outsource security to specialists.[43]

Regional variations present opportunities. North American companies show highest exposure to cyber risks (37% report significant breach costs), driving investment, while technology sectors lead in AI security adoption.[44] However, challenges persist: Skills shortages (41% cite lack of AI expertise as a barrier), regulatory compliance needs, and concerns about quantum computing threats (though only 3% have implemented quantum-resistant measures) will shape investment success.[45]

4. AI Infrastructure Beyond Chips: Data Centers, Power, and Services

While Nvidia and other semiconductor companies captured early AI infrastructure investment, the next wave of opportunities lies in the ecosystem supporting AI compute: data centers, energy infrastructure, cooling systems, networking equipment, and AI services. This subsector is projected to account for over $330 billion in AI-optimized server spending alone by 2026, with additional tens of billions in supporting infrastructure.[46]

The investment thesis is structural: AI training and inference require exponentially more computational power than previous workloads, straining existing data center capacity and energy grids. Microsoft, Alphabet, Meta, and Amazon are collectively spending $370-380 billion on AI data centers and infrastructure in 2025, with growth accelerating into 2026.[47] This creates massive downstream opportunities for companies providing the physical infrastructure, power systems, and services that make hyperscale AI computing possible.

Data Center Construction and Real Estate: AI data centers have fundamentally different requirements than traditional facilities—higher power densities, advanced cooling systems, and proximity to power sources. Companies specializing in AI-optimized data center design, construction, and real estate are experiencing unprecedented demand. The U.S. Energy Department's $1 billion partnership with AMD for AI supercomputing infrastructure illustrates government support for this buildout.[48]

Energy and Utilities: AI's energy consumption is creating investment opportunities in power generation and grid infrastructure. Data centers powering AI workloads account for much of U.S. GDP growth in early 2025, but utilities are struggling to meet demand, with some seeking rate increases due to supply shortages.[49] Investments in renewable energy (to meet sustainability commitments), grid infrastructure, and innovative cooling technologies (liquid cooling, immersion cooling) are positioned to benefit.

Networking and Connectivity: AI training clusters require ultra-high-bandwidth networking to connect thousands of GPUs. Companies providing 400G and 800G Ethernet switches, optical transceivers, and interconnect technologies are seeing surging demand. TechInsights predicts datacenter accelerators will exceed $300 billion by 2026, driven by innovations in co-packaged optics and advanced networking.[50]

AI Services and Integration: Beyond hardware, the services layer—consulting, integration, implementation, and managed AI services—represents a substantial market. Companies helping enterprises deploy AI infrastructure, optimize workloads, and manage hybrid cloud-edge architectures are capturing value as businesses lack in-house expertise. Capgemini's $3.3 billion acquisition of WNS and similar M&A activity signals strong growth in AI services.[51]

Geographic dynamics matter here too. While North America leads in AI infrastructure spending, Asia-Pacific is experiencing the fastest growth, driven by government subsidies and strategic AI investments in China and India.[52] Supply chain risks—particularly around semiconductor manufacturing and U.S.-China tensions—add complexity but also create opportunities for companies diversifying production or developing domestic capabilities.

Venture Capital and Private Markets: Where the Smart Money Is Really Going

The M&A and Consolidation Wave

Venture capital's role in AI is evolving rapidly as the market matures. While headline funding numbers remain impressive—$192.7 billion in AI investments through Q3 2025—the underlying dynamics reveal a strategic shift toward consolidation, selectivity, and exits rather than indiscriminate seed funding.[53]

Venture capital firms are shifting from horizontal AI platforms to specialized, revenue-generating AI companies

Venture capital firms are shifting from horizontal AI platforms to specialized, revenue-generating AI companies

Foley & Lardner's analysis predicts a surge in M&A and secondary transactions in 2026, as investors prioritize mature companies with credible compliance plans and proven revenue models over early-stage startups with ambitious visions but no customers.[54] This trend is already visible: Average late-stage deal sizes have tripled to $1.55 billion year-over-year, while early-stage seed funding shows no growth.[55] The message is clear: Capital is flowing to winners, not experiments.

Several factors are driving this consolidation:

The Horizontal AI Shakeout: Generalist AI platforms that don't solve specific industry problems are losing funding. Investors have learned that "AI for everyone" rarely works—successful AI companies typically focus on vertical markets (healthcare diagnostics, financial fraud detection, supply chain optimization) where they develop deep domain expertise and defensible competitive advantages.[56] Foley & Lardner predicts significant failures among horizontal startups in 2026 as funding dries up.

Revenue Discipline: The shift from valuation based on potential to valuation based on actual revenue is accelerating. Companies demonstrating product-market fit, recurring revenue streams, and paths to profitability are commanding premium valuations, while those still burning cash on customer acquisition face down rounds or shutdowns. Generative AI startups raised over $2 billion in 2023, but many are now struggling to monetize their technology.[57]

Strategic Acquisitions: Tech giants and established enterprises are acquiring AI capabilities rather than building them internally. This creates lucrative exit opportunities for startups with proven technology, trained teams, and customer bases. CB Insights reports an 8% quarter-over-quarter increase in M&A activity, with 2,324 transactions in Q3 2025, heavily weighted toward AI startups, fintech, and healthcare.[58]

Exit Market Revival: IPO and acquisition markets are strengthening after years of drought. Global exit values reached $149.9 billion in Q3 2025—the highest since Q4 2021—driven by renewed appetite for technology offerings and corporate acquirers seeking AI capabilities.[59] KPMG predicts this exit activity will accelerate into 2026, creating liquidity for venture investors and enabling new funding cycles.

Geographic and Sector Concentration

Venture capital in AI remains heavily concentrated geographically, creating both risks and opportunities. The United States dominates with 97% of global generative AI deal value and 85% of total AI funding in 2025, driven by Silicon Valley's ecosystem and regulatory advantages.[60] This concentration means U.S.-focused VC firms have disproportionate access to deal flow, but it also creates vulnerability to U.S.-specific policy changes or market corrections.

Europe is gaining ground in specific niches, particularly robotics (over $1 billion invested in 2025), quantum computing, and privacy-focused AI, but overall captures only 2% of GenAI deal value globally, with just three AI unicorns compared to 29 in the U.S.[61] For investors, European AI companies may offer value opportunities given lower valuations, but they face headwinds from fragmented markets and less developed venture ecosystems.

Asia, particularly China, presents a complex picture. While geopolitical tensions have muted overall investment ($16.8 billion in Q3 2025), government subsidies and strategic funds are supporting specific sectors like autonomous vehicles, consumer AI, and semiconductor self-sufficiency.[62] Investors willing to navigate regulatory complexities may find opportunities in Asian edge computing and vertical AI applications as these markets develop.

The Investor Playbook for 2026

For limited partners, angel investors, and institutions considering AI venture exposure, several strategies are emerging:

Focus on AI Application Layer, Not Infrastructure: While chip and cloud infrastructure dominated early AI investment returns, these markets are now crowded and capital-intensive. The application layer—companies using AI to solve specific problems in healthcare, finance, manufacturing, legal, etc.—offers better risk-adjusted returns with lower capital requirements and clearer paths to revenue.[63]

Prioritize Companies with Defensible Data Moats: In AI, data is often more valuable than algorithms. Companies with proprietary datasets, exclusive partnerships that provide data access, or network effects that generate continuous data creation have sustainable competitive advantages. Generic AI models trained on public data face commoditization risk.[64]

Demand Revenue Metrics Over Vanity Metrics: User growth and engagement matter less than annual recurring revenue (ARR), customer acquisition costs (CAC), lifetime value (LTV), and gross margins. The "growth at any cost" mentality is dead; profitability paths are essential.[65]

Invest in AI Services and Enablement: The "picks and shovels" strategy remains valid, but it's shifting from chips to services—consulting firms helping enterprises implement AI, integration platforms connecting AI to existing systems, and tools for managing AI lifecycle and governance.[66]

Enterprise ROI Expectations and Investment Implications

The ROI Reality Check

As enterprises move from pilot projects to production AI deployments, return on investment has become the central question shaping 2026 investment decisions. The data presents a mixed picture: While some companies report transformative gains, many struggle to demonstrate measurable financial impact, creating pressure on vendors to prove value and investors to identify companies delivering real results.

Forrester's warning that enterprises may delay 25% of AI spending reflects this ROI challenge.[67] Only 15% of AI decision-makers report earnings increases from their AI investments over the past year—a surprisingly low figure given the hype.[68] SAS analysts describe 2026 as the year of the "Great AI Reality Check," where projects without measurable impact face shuttering and organizations demand accountability over innovation theater.[69]

Yet the successful deployments tell a different story. Companies implementing agentic AI report substantial gains:

- 20-35% lower operational costs through automation of routine tasks

- 20-30% productivity gains from AI-augmented workers

- 10-30% revenue increases from AI-enabled products and services

- $1-4 saved per dollar spent on cost reduction initiatives (ROI of 100-400%)

- 90%+ accuracy in automated data extraction and classification tasks[70]

Healthcare provides compelling examples: AI-powered imaging prevents an estimated 2.5 million diagnostic errors annually, while case studies show 42% time savings in administrative documentation.[71] Financial services expects $97 billion in AI investments by 2027, with 70% of executives anticipating revenue growth from fraud prevention and customer service enhancements.[72] Retail companies report 9.7% increases in sales conversions and tens of millions in gross profit gains from AI-driven customer engagement.[73]

What Success Looks Like: Sector-Specific ROI Benchmarks

Investment opportunities are strongest in sectors demonstrating clear ROI:

IT and Telecommunications: 53% of businesses use AI for cybersecurity, with measurable reductions in breach frequency and response time. Agentic AI in IT operations delivers 50% faster response to disruptions and data-driven improvements in infrastructure management.[74] These concrete metrics make IT applications attractive investment targets.

Healthcare and Life Sciences: AI applications in diagnostics, patient monitoring, and drug discovery generate up to $150 billion in annual savings by 2026, with 32% of pharma and medtech leaders already scaling generative AI.[75] Companies demonstrating clinical efficacy and regulatory approval pathways command premium valuations.

Financial Services: 70% of banking and insurance executives report efficiency gains from AI, with specific applications in fraud detection (preventing losses), credit assessment (reducing defaults), and customer service (lowering costs) showing 10-40% improvements.[76] Investment opportunities cluster around companies with proven financial institution deployments.

Manufacturing and Supply Chain: AI drives 25% faster delivery times and supply chain optimization, with the market projected to $230.95 billion by 2034.[77] Companies offering autonomous logistics, predictive maintenance, and quality control solutions are attracting strategic investments from manufacturers seeking operational efficiency.

Legal and Professional Services: AI reduces legal research time by 60% in firms like BakerHostetler, with document review, contract analysis, and due diligence applications showing immediate time savings.[78] This creates opportunities in legal tech startups demonstrating billable hour reductions or error rate improvements.

The Five Pillars of AI ROI

Gartner's framework for achieving AI ROI emphasizes five capabilities that successful companies develop:[79]

- Strategic AI Roadmaps: Clear alignment between AI investments and business objectives, with executive sponsorship and measurable KPIs

- Value Targets and Measurement: Rigorous tracking of AI's business impact using A/B testing, baseline comparisons, and financial metrics

- Upskilling and Change Management: Training workforces to collaborate with AI, addressing the 35% of organizations citing skills gaps as barriers

- Data Governance and Quality: Ensuring AI has access to clean, relevant data with appropriate privacy and security controls

- Resource Prioritization: Focusing on high-impact use cases rather than spreading resources across countless pilots

For investors, these pillars provide a filter: Companies that excel in these areas are more likely to achieve returns and sustain competitive advantages. Due diligence should assess not just a company's AI technology but its implementation methodology, customer success processes, and measurement frameworks.

Strategic Investment Frameworks for 2026

Portfolio Construction in a Maturing AI Market

Building an AI-focused investment portfolio for 2026 requires balancing exposure across risk levels, subsectors, and company maturities. The following framework synthesizes institutional investor approaches:

Core Holdings (40-50% of AI allocation): Established AI infrastructure and service companies with proven revenue models, strong cash flow, and defensive competitive positions. This includes:

- Hyperscale cloud providers (Microsoft Azure, Google Cloud, Amazon AWS) offering AI services with demonstrated growth

- Semiconductor companies (Nvidia, AMD, Intel) with diversified AI chip portfolios spanning training and inference

- Enterprise software companies (Salesforce, ServiceNow, Adobe) successfully integrating AI into existing products

These core holdings provide stability and capitalize on continued AI adoption without excessive valuation risk.

Growth Positions (30-40% of AI allocation): Higher-growth subsectors with strong tailwinds but more volatility:

- Edge computing infrastructure companies (hardware, software, and services)

- Cybersecurity firms with AI-driven threat detection and response capabilities

- Agentic AI platforms with demonstrated enterprise traction and recurring revenue

- AI services and consulting firms capturing implementation spending

These positions offer asymmetric upside if growth projections materialize but carry execution risk.

Venture/Opportunistic (10-20% of AI allocation): Early-stage companies and emerging subsectors with transformative potential:

- Vertical-specific AI applications in healthcare, finance, legal, and manufacturing

- Novel AI architectures and approaches (neuromorphic computing, quantum-AI hybrid)

- Geographic plays in underinvested regions (European robotics, Asian edge computing)

- Infrastructure components (energy, cooling, networking) benefiting from AI buildout

This allocation provides exposure to potential category creators while limiting overall portfolio risk given higher failure rates.

Hedges and Alternatives (0-10% of AI allocation): Positions that benefit from AI market corrections or related trends:

- Cybersecurity pure-plays protecting against AI-enabled threats regardless of AI adoption rates

- Energy and utilities capturing power demand from AI data centers

- AI ethics and governance companies positioning for regulatory tailwinds

- Cash or short-duration bonds providing dry powder for opportunistic deployment

Due Diligence Checklist for AI Investments

Before allocating capital to any AI company or subsector, rigorous due diligence should assess:

Business Model and Revenue Quality:

- Is revenue recurring (SaaS, subscriptions) or transactional?

- What percentage comes from AI products versus legacy offerings?

- Are customers expanding usage (net revenue retention >110%)?

- Does the company have product-market fit in a specific vertical?

Competitive Position and Differentiation:

- What defensible competitive advantages exist (data moats, network effects, switching costs)?

- How reliant is the company on third-party AI models (OpenAI, Anthropic) versus proprietary technology?

- Can competitors replicate the offering easily, or are there technical or regulatory barriers?

Financial Health and Efficiency:

- What is the path to profitability or EBITDA positivity?

- How capital-efficient is growth (CAC payback period, LTV/CAC ratio)?

- Is burn rate sustainable through multiple funding cycles?

- For public companies, do valuations reflect realistic growth expectations?

Execution and Governance:

- Does management have domain expertise and successful exits?

- Is there robust AI governance addressing bias, transparency, and safety?

- How does the company measure and communicate AI ROI to customers?

- Are there regulatory risks (data privacy, industry-specific rules)?

Market Timing and Catalysts:

- Is the market ready for this solution, or is it too early?

- Are there near-term catalysts (product launches, regulatory changes, major customer wins)?

- What could go wrong (technology risk, market shifts, competitive threats)?

Navigating Valuation Challenges

AI valuations present particular challenges given rapid growth rates, uncertain competitive dynamics, and hype cycles. Several valuation approaches can help:

Revenue Multiples with Growth Adjustments: For AI software companies, price-to-sales ratios adjusted for growth rates (the "Rule of 40") provide context. Companies growing revenue 50%+ per year with 20-30% operating margins may justify 10-15x revenue multiples, while slower growers trade at 3-6x.

Comparable Company Analysis: Compare AI companies to peers in their specific subsector (edge computing, cybersecurity, agentic AI) rather than broad "AI" comparisons, as growth rates and margins vary dramatically.

Discounted Cash Flow with Scenario Analysis: For established AI companies, DCF models with multiple scenarios (bear, base, bull) help assess risk-reward. Key assumptions include market penetration rates, competitive pricing pressure, and gross margin sustainability as markets mature.

Venture Capital Stage-Appropriate Metrics: Early-stage AI companies should be valued on user growth, engagement, and technical milestones rather than revenue. However, Series B and beyond require demonstrated revenue traction and unit economics.

Avoiding Bubble Indicators: Watch for warning signs like extreme forward multiples (>30x revenue for companies growing <100%), circular investments (AI companies investing in each other), excessive insider selling, and revenue recognition issues.

Risks, Challenges, and Contrarian Perspectives

The Bear Case: Why AI Might Disappoint Investors

No investment outlook is complete without examining downside scenarios. Several credible analysts warn that AI investment returns may disappoint:

The Productivity Paradox: Goldman Sachs research questions whether AI will generate productivity gains commensurate with investment levels, noting that corporate inertia and integration challenges often delay or prevent technology adoption even when benefits are proven.[80] History shows technology revolutions often take decades to deliver economic returns—electricity took 40+ years to drive productivity gains, and computers took similar timeframes.[81]

The Commoditization Risk: As AI models improve and become widely available (via open-source releases and API access), differentiation may erode, compressing margins and returns. Companies building on third-party AI platforms (OpenAI, Anthropic) face particular risk if those platforms capture most of the value or if costs remain high.[82]

The Energy and Sustainability Wall: AI's exponential energy consumption may hit physical limits as utilities struggle to provide power and concerns about carbon emissions grow. If data center expansion stalls due to energy constraints or sustainability backlash, AI growth could decelerate faster than expected.[83]

The Regulatory Hammer: Government intervention—whether through AI safety regulations, antitrust actions against dominant players, or data privacy restrictions—could reshape the competitive landscape and limit growth. The EU AI Act, potential U.S. regulations, and China's AI governance all create regulatory uncertainty.[84]

The Geopolitical Fragmentation: U.S.-China tensions, semiconductor supply chain disruptions, and data sovereignty requirements could fragment the global AI market, increasing costs and limiting scalability for companies dependent on international operations.[85]

These risks don't invalidate the AI investment thesis but underscore the importance of diversification, selectivity, and continuous monitoring of assumptions.

The Bull Case: Why AI May Exceed Expectations

Conversely, several factors could drive AI returns beyond current projections:

Accelerating Breakthroughs: AI is improving AI, creating a potential exponential growth curve. As AI systems help design better AI architectures, generate synthetic training data, and automate research, the pace of advancement could accelerate rather than following historical technology adoption curves.[86]

Winner-Take-Most Dynamics: Network effects and data flywheels may create more durable competitive advantages than bears expect. Companies that achieve market leadership in specific AI applications may sustain high margins and growth far longer than in previous software markets.[87]

Underestimated Addressable Markets: Many AI applications are still in early stages. If AI successfully penetrates markets like education, government, agriculture, and construction—where adoption lags—the total addressable market could dwarf current estimates.[88]

The Services Multiplier: For every dollar spent on AI technology, enterprises may spend three to five dollars on services, integration, and change management. This creates a massive services opportunity beyond the core technology investments already projected.[89]

Conclusion: Navigating AI's Next Chapter

As we stand at the threshold of 2026, AI investing is entering a new phase—one characterized by maturity, discipline, and specialization rather than indiscriminate enthusiasm. The easy money from betting on obvious winners like Nvidia and Microsoft may be behind us, but opportunities abound for investors willing to dig deeper into subsectors where growth potential remains high and valuations more reasonable.

Edge computing's $50+ billion market, agentic AI's 45% growth rate, cybersecurity's defensive positioning, and infrastructure's essential role in the AI ecosystem offer compelling risk-reward profiles for 2026. Venture capital's shift toward revenue-generating companies with proven business models, rather than experimental pilots, creates exit opportunities and validates that real value is being created beyond hype.

Yet success requires discipline. The ROI reality check means investments must target companies demonstrating measurable financial impact, not just impressive demonstrations. Portfolio construction should balance core holdings in established AI leaders with growth positions in specialized subsectors and opportunistic allocations to emerging categories. Due diligence must assess competitive moats, revenue quality, and realistic path to profitability rather than accepting growth narratives at face value.

The risks are real—valuation excesses, competitive commoditization, energy constraints, regulatory intervention—but so are the opportunities. AI is not merely another technology wave; it represents a fundamental shift in how humans interact with information, make decisions, and organize economic activity. For investors who navigate this transition with clear-eyed analysis rather than euphoria or fear, 2026 offers the potential for substantial, sustainable returns.

The smart money isn't abandoning AI—it's refining where and how it invests. Those who follow suit, focusing on specialized subsectors with demonstrable ROI, diversified exposure across the AI value chain, and rigorous risk management, are positioned to capture the next wave of value creation in humanity's most transformative technology transition.

References and Citations

- "Top 6 AI Markets in $1.5 Trillion Industry: AI Spending in 2026 to Hit $2 Trillion" - Gartner via CRN, 2025

- "AI Is Dominating 2025 VC Investing, Pulling in $192.7 Billion" - Bloomberg, October 2025

- "Forbes Best AI Stocks to Buy 2026" - Forbes Investor Hub, 2025

- "The Outlook for AI Adoption as Advancements in the Technology Accelerate" - Goldman Sachs Research, 2025

- "Edge AI Market Size, Share & Trends Analysis Report 2030" - Grand View Research, 2024

- "AI Agents Market Size, Share, Growth & Trends 2030" - Grand View Research, 2025

- "Global Cyber Risk Trends 2026" - PwC, October 2025

- "What's New in Venture Capital: Update on Q3 2025 Venture Capital Trends" - Foley & Lardner, 2025

- "AI Spending May Slow Down as ROI Remains Elusive" - CIO.com, 2025

- "SAS Predictions 2026: The Great AI Reality Check" - SAS Institute, November 2025

- "CFOs Shift AI Budgets to Agents in 2026" - PYMNTS, 2025

- "CFOs Shift AI Budgets to Agents in 2026" - PYMNTS Intelligence, 2025

- "Gartner: Agentic AI to Define Next Wave of Enterprise ROI" - Technology Magazine, 2025

- "Data Center AI Boom Masks Potential US Recession, Analyst Warns" - CNBC, October 2025

- "AI Infrastructure Boom Masks Potential US Recession" - CNBC Analysis, 2025

- "AI Stocks 2025: Investor Guide" - IO Fund, 2025

- "Generative AI VC Funding $49.2B H1 2025" - EY Report, June 2025

- "Three Trends That Will Define AI in 2026" - Foley & Lardner Insights, 2025

- "Edge AI Market: AI Edge Computing to Hit $56.8 Billion by 2030" - BCC Research, 2025

- "Uncovering AI Hidden Gems: Niche Subsectors Poised to Outperform 2025" - AInvest, 2025

- "AI in Edge Computing Market to Surpass USD 83.86 Billion by 2032" - PRNewswire, 2025

- "Edge AI Market Report: Industry Analysis and Forecast to 2030" - Grand View Research, 2024

- "AI Edge Computing Market: Industry Analysis by Technavio" - Technavio Report, 2025

- "Edge AI Market Report 2024: Regional Analysis" - Grand View Research, 2024

- "AI Agents Market Size & Growth Report 2030" - Grand View Research, 2025

- "AI Agent Statistics: Adoption and Implementation Trends" - Pragmatic Coders, 2025

- "Gartner Forecasts: AI Agents in Enterprise Applications by 2026" - Gartner Research, 2025

- "AI Agent Statistics: Efficiency Gains Across Industries" - McKinsey via Pragmatic Coders, 2025

- "Agentic AI Adoption Rates, ROI, and Market Trends" - OneReach.ai Blog, 2025

- "AI Agent Statistics: BCG Growth Forecasts" - BCG via Pragmatic Coders, 2025

- "Venture Capital Trends: AI and Robotics Investment 2025" - Wise Blog, 2025

- "Agentic AI Predictions: Guardian Agents and Oversight" - Atera, 2025

- "AI Agent Statistics: Trust and Security Challenges" - Pragmatic Coders, 2025

- "AI Agents Statistics: Implementation Hurdles" - Warmly.ai, 2025

- "AI Cybersecurity Trends: Market Projections to 2030" - SentinelOne, 2025

- "The AI Cyber Arms Race: Forecasting Cybersecurity's AI-Driven Future in 2026" - TokenRing via Financial Content, 2025

- "Google Cybersecurity Forecast 2026: AI to Supercharge Cybercrime" - Help Net Security, November 2025

- "PwC Global Digital Trust Insights 2026: AI Investment Priorities" - PwC Press Release, October 2025

- "AI Security Trends: Adoption and Implementation Statistics" - Lakera.ai Blog, 2025

- "Global Cyber Risk Trends 2026: AI-Enabled Threat Hunting" - PwC via Help Net Security, October 2025

- "Google Cybersecurity Forecast 2026: Identity Debt and AI Fragmentation" - Help Net Security, 2025

- "AI Security Trends: Enterprise Preparedness Statistics" - Lakera.ai, 2025

- "2026 MSP Outlook: Growth Amid AI and Cybersecurity Trends" - VoIP Review, November 2025

- "PwC Digital Trust Insights: Regional Cyber Risk Exposure" - PwC, 2025

- "Top Cybersecurity Trends and Predictions for 2026" - Splashtop Blog, 2025

- "Top 6 AI Markets: AI-Optimized Server Spending Projections" - Gartner via CRN, 2025

- "Tech AI: Google, Meta, Amazon, Microsoft Spending on AI Infrastructure" - CNBC, October 2025

- "2025's Incredible AI Spending Frenzy: US Forms $1 Billion Partnership with AMD" - Forbes, October 2025

- "Data Center AI Boom and US Economy Jobs Impact" - WIRED, 2025

- "Outlook Summit Series 2026: AI Market Forecasts" - TechInsights, 2025

- "Artificial Intelligence H1 2025 Global Report: M&A Activity" - Ropes & Gray, August 2025

- "AI Market Growth 2026 Projections: Regional Analysis" - Amity Solutions Blog, 2025

- "AI Is Dominating 2025 VC Investing: Q3 2025 Data" - Bloomberg via PitchBook, October 2025

- "Three Trends That Will Define AI in 2026: M&A and Secondary Transactions" - Foley & Lardner, 2025

- "Generative AI VC Funding: Deal Size Analysis H1 2025" - EY Report, June 2025

- "Three Trends That Will Define AI in 2026: Horizontal AI Shakeout" - Foley & Lardner, 2025

- "AI Market Growth 2026: Generative AI Funding Statistics" - Amity Solutions, 2025

- "What's New in Venture Capital: Q3 2025 M&A Trends" - Foley & Lardner via CB Insights, 2025

- "Global VC Investment Rises in Q3 2025: Exit Market Analysis" - KPMG, October 2025

- "Generative AI VC Funding: Geographic Breakdown H1 2025" - EY Ireland Newsroom, June 2025

- "Generative AI VC Funding: European AI Unicorn Statistics" - EY Report, 2025

- "Global VC Investment Q3 2025: Asia-Pacific Analysis" - KPMG Media Release, 2025

- "AI Investment Landscape 2025: Opportunities in Volatile Market" - FTI Consulting Insights, 2025

- "Unlocking Value from Technology and AI for Institutional Investors" - McKinsey, 2025

- "AI Investment Strategies for Financial Markets: Revenue Discipline" - Straits Financial Insights, 2025

- "Artificial Intelligence H1 2025 Global Report: AI Services Sector" - Ropes & Gray, 2025

- "AI Spending May Slow Down as ROI Remains Elusive" - CIO.com, 2025

- "AI Spending Delays: Forrester ROI Analysis" - CIO.com citing Forrester, 2025

- "SAS Predictions 2026: Great AI Reality Check" - SAS Press Release, November 2025

- "Agentic AI Adoption Rates, ROI, and Market Trends: Financial Metrics" - OneReach.ai, 2025

- "Agentic AI ROI: Healthcare Savings and Efficiency Gains" - OneReach.ai citing industry data, 2025

- "Agentic AI Market Trends: Financial Services Investment Projections" - OneReach.ai, 2025

- "Agentic AI ROI: Retail and E-Commerce Case Studies" - OneReach.ai, 2025

- "ROI of Implementing Agentic AI in Enterprise IT: Metrics That Matter" - Swish.ai, 2025

- "Agentic AI Adoption: Healthcare and Life Sciences Statistics" - OneReach.ai and Artificial Intelligence H1 2025 Report, 2025

- "Agentic AI Financial Services: Executive Survey Results" - OneReach.ai, 2025

- "Agentic AI Manufacturing: Market Projections to 2034" - OneReach.ai citing industry forecasts, 2025

- "Agentic AI Legal Services: Time Savings Case Studies" - OneReach.ai, 2025

- "Gartner Agentic AI: Five Pillars Framework for Enterprise ROI" - Technology Magazine citing Gartner, 2025

- "The Outlook for AI Adoption: Productivity Paradox Analysis" - Goldman Sachs Insights, 2025

- "AI Investment Forecast: Historical Technology Adoption Comparisons" - Goldman Sachs Research, 2025

- "Opinion: Investing in the New AI Industrial Order" - Institutional Investor, 2025

- "Data Center AI Boom and Energy Grid Constraints" - WIRED, 2025

- "AI Investment Landscape 2025: Regulatory Risks" - FTI Consulting, 2025

- "Outlook Summit Series 2026: Geopolitical AI Market Factors" - TechInsights, 2025

- "The Outlook for AI Adoption: Self-Improving AI Systems" - Goldman Sachs Insights, 2025

- "Institutional Investors in the Age of AI: Data Opportunity" - State Street Alpha Insights, 2025

- "AI Market Growth 2026: Underestimated Addressable Markets" - Amity Solutions Analysis, 2025

- "Meta's Big AI Spending Blitz Will Continue Into 2026: Services Multiplier" - CNBC, July 2025

This analysis is for informational purposes only and does not constitute investment advice. AI markets are highly volatile, and investment outcomes depend on numerous factors beyond the scope of this article. Conduct thorough due diligence and consult with financial advisors before making investment decisions.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Markets and competitive dynamics can change rapidly in the technology sector. Taggart is not a licensed financial advisor and does not claim to provide professional financial guidance. Readers should conduct their own research and consult with qualified financial professionals before making investment decisions.

Taggart Buie

Writer, Analyst, and Researcher