The 2026 AI Investment Playbook: What Wall Street Expects After the $800 Billion Correction

After AI stocks shed $800 billion in the 2025 correction, Wall Street's 2026 playbook reveals surprising bullishness. With Big Tech's AI capex exceeding $405 billion, analyst price targets pointing to 40% upside in Meta and Alphabet, and agentic AI delivering 10x ROI, discover where the smart money is positioning for the AI revolution's next phase.

The 2026 AI Investment Playbook: What Wall Street Expects After the $800 Billion Correction

The dust is settling on one of the most dramatic market corrections in artificial intelligence history. After a wild 2025 that saw AI stocks collectively shed over $800 billion in value during peak volatility, Wall Street analysts, institutional investors, and savvy money managers are publishing their 2026 playbooks—and they're surprisingly bullish.

Despite the turbulence, the message from the smart money is clear: the AI revolution hasn't stalled. It's simply maturing. And with that maturity comes the most significant investment opportunity since the early days of cloud computing.

Here's your comprehensive guide to navigating the AI investment landscape in 2026, backed by Wall Street's latest forecasts, institutional positioning data, and the hard numbers that separate winners from pretenders.

The Post-Correction Reality: Where We Stand

Nearly 80% of North American institutional investors anticipated a market pullback in 2026, and they were partially right. The AI sector experienced its worst drawdown since the pandemic, driven by concerns over excessive capital expenditures, unclear monetization paths, and valuation extremes that made even the dot-com bubble look modest.

But here's what changed everything: the fundamentals didn't break.

While stock prices corrected sharply, the underlying drivers of AI adoption—enterprise spending, infrastructure buildout, and productivity gains—not only held steady but accelerated. Big Tech's combined AI capital expenditures are projected to exceed $405 billion in 2025, up 62% year-over-year, with further increases expected in 2026.

Microsoft's CFO signaled that capex growth would accelerate in fiscal 2026, not slow down, with estimates suggesting a minimum of $94 billion (potentially reaching $140 billion including leases). Google's capital expenditures, initially forecast at $60 billion for 2025, were repeatedly revised upward to $91-93 billion, with a "substantial increase" planned for 2026.

The correction wasn't a crisis of confidence in AI—it was a recalibration of expectations.

Wall Street's 2026 Price Targets: The Magnificent Seven and Beyond

Nvidia (NVDA): Still the Infrastructure King

Despite controlling approximately 90% of the AI GPU market, Nvidia faced its share of volatility. But Wall Street's consensus remains firmly bullish:

- Current Position: Market dominance in AI chips, with the Blackwell Ultra architecture delivering significant performance gains for large reasoning models

- 2026 Catalysts: OpenAI's planned $100 billion investment (including initial $10 billion Nvidia system purchase), enterprise AI adoption reaching critical mass, and the MI450 cluster deployments scheduled for H2 2026

- Analyst Consensus: Average 12-month price target around $210, with bulls projecting up to $250

- Risk Factors: Competition from AMD's MI350 series and hyperscalers' custom silicon (Google TPUs, Amazon Trainium) could pressure margins

Meta Platforms (META): The Undervalued AI Giant

Meta has emerged as one of the most compelling AI value plays heading into 2026:

- Valuation Edge: P/S ratio of 7.2, significantly lower than Nvidia (19.4), Microsoft (13.2), and Alphabet (7.2)

- AI Monetization: AI-driven advertising tools contributing over $60 billion in annual revenue (approximately one-third of total sales)

- Analyst Targets: Median target of $850 per share among 73 analysts, implying 40% upside from current levels

- Investment Thesis: 26% YoY revenue growth, 43% operating margin, and $44 billion in free cash flow demonstrate operational excellence while trading at a discount

Alphabet (GOOGL): The Multi-Front AI Bet

Google's diversified AI approach positions it uniquely for 2026:

- Competitive Advantage: Leadership in AI infrastructure and large language models driving cloud market share gains

- TPU Strategy: Heavy investment in custom Tensor Processing Units (Ironwood v7 offers 10x computing power vs. v5p) to reduce dependency on Nvidia and improve margins

- Cloud Momentum: Google Cloud's revenue grew 33.5% YoY to $15.1 billion, with AI workloads becoming increasingly significant

- Analyst Outlook: Median target of $330 per share (18% upside), with 15% annual earnings growth projected through 2029

- 2026 Prediction: Some analysts believe Google could surpass Apple in market capitalization by year-end 2026

AMD (AMD): The Challenger Gaining Ground

AMD's aggressive push into AI chips is paying dividends:

- Strategic Wins: Long-term OpenAI agreement for large-scale MI450 cluster purchases in H2 2026

- Performance Claims: MI325X offering market-leading inference performance, with MI300 series matching or exceeding Nvidia's H100 for 70B LLM inference

- Financial Projection: 66% annualized free cash flow growth through 2029

- Price Targets: Bank of America and Canaccord Genuity raised targets to $60

- Software Moat: ROCm ecosystem improving as credible CUDA alternative, reducing Nvidia lock-in

Microsoft (MSFT): The Enterprise AI Standard

Microsoft's position as OpenAI's primary partner and Azure's dominance in enterprise AI provides powerful tailwinds:

- Azure AI Growth: Leading enterprise AI adoption through ChatGPT integration, Copilot deployment, and cloud infrastructure

- Capital Commitment: Among Nvidia's top three hyperscaler customers, with ongoing massive AI infrastructure investments

- 2026 Outlook: Continued strength in cloud services and AI tools, though growth may moderate compared to pure-play AI companies

- Valuation: Premium pricing reflects market-leading position, but enterprise stickiness justifies multiples

The Subsector Thesis: Infrastructure vs. Applications vs. Chips

AI Infrastructure: The $1 Trillion Backbone

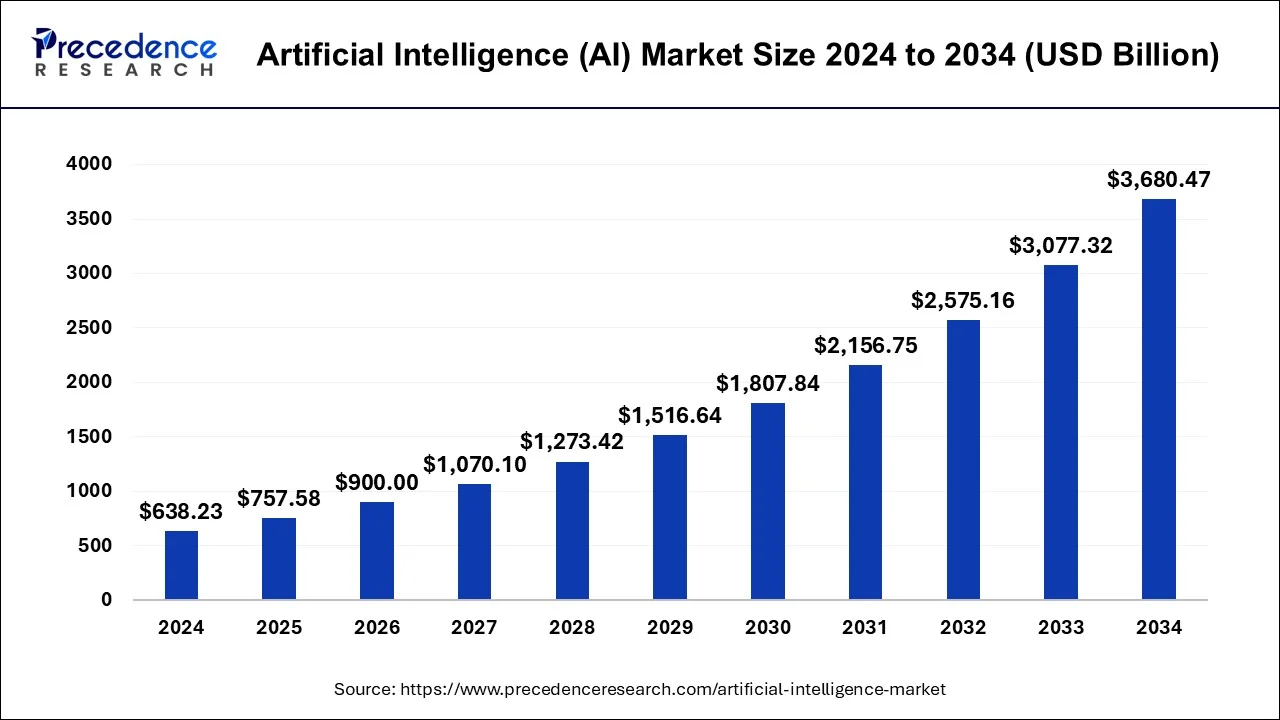

The global AI infrastructure market is projected to reach $1 trillion by 2030, with 2026 representing a critical inflection point:

Investment Highlights:

- Data Center Boom: AI-optimized IaaS spending will exceed $37.5 billion in 2026, more than doubling from 2025's $18.3 billion

- Inferencing Dominance: Over 55% of AI-optimized IaaS spending in 2026 will be driven by inference (not training), signaling the shift from model development to deployment at scale

- Power & Cooling: AI data centers require 40-100 kilowatt racks (some exceeding 100kW), driving $720 billion in grid infrastructure spending through 2030

- Edge Computing: Capacity projected to grow 20% annually through 2027, with latency-sensitive applications like autonomous vehicles driving demand

Key Players:

- Super Micro Computer (SMCI): Direct liquid cooling technology leader, with AI server market share projected to grow from 10% (2023) to 17% by 2026 (Bank of America) or 23% (KeyBanc)

- Vertiv, Eaton: Power infrastructure and cooling solutions benefiting from data center buildout

- Digital Realty, Equinix: REITs with AI-ready data center portfolios

AI Applications: The Monetization Wave

After years of infrastructure buildup, 2026 marks the year enterprise AI applications demonstrate clear ROI:

Agentic AI Revolution:

- Market Size: AI agents market valued at $5.40 billion in 2024, projected to reach $50.31 billion by 2030 (45.8% CAGR)

- Enterprise Adoption: 40% of enterprise applications will incorporate task-specific AI agents by end of 2026 (Gartner)

- ROI Metrics: Organizations seeing 5x-10x returns per dollar invested in agentic AI

- Key Sectors: Healthcare (68% using AI agents), financial services ($97 billion projected investments by 2027), retail (41% investing)

Investment Opportunities:

- ServiceNow (NOW): Targeting $1 billion in AI-related revenue by 2026

- SoundHound AI (SOUN): Conversational AI specialist, Q3 2025 revenue up 68% YoY to $42 million, targeting 40% growth in 2026

- Tempus AI (TEM): AI-driven precision medicine, first positive adjusted EBITDA in Q3 2025, 84.7% YoY revenue growth

- Salesforce (CRM): Enterprise AI adoption through Agentforce and multi-agent orchestration

Semiconductor Battleground: The Competition Heats Up

The AI chip market in 2026 will see intensified competition beyond Nvidia's dominance:

AMD's Challenge:

- MI350 series (3nm process) shipping in 2025, MI400 "Helios" racks targeting 2026 hyperscale adoption

- Strategic acquisitions (Untether AI team, Brium) strengthening compiler and inference capabilities

- Projected Data Center GPU Revenue: Significantly higher than Intel's Gaudi 3 sales guidance

Intel's Comeback Attempt:

- Gaudi 3 shipping in racks from Dell, HPE, Supermicro

- Open ecosystem strategy supporting PyTorch, TensorFlow, Hugging Face

- Challenge: Slower market penetration than competitors, internal governance issues

Qualcomm's Entry:

- AI200 (2026) and AI250 (2027) data center chips focusing on inference

- Cost-effective rack-scale systems with 768GB memory capacity

- Strategy: Power efficiency and price competition targeting cloud service providers

Custom Silicon Trend:

- Google TPUs: Ironwood (v7) offers 4x speed vs. Trillium, 10x computing power vs. v5p

- Amazon Trainium: Trainium2 for Project Rainier (Anthropic models), Trainium3 in development

- Microsoft Maia: Maia 100 for Azure and OpenAI models

Market Outlook: Global semiconductor market forecast to reach ~$800 billion in 2026, up from $728 billion in 2025

Buy the Dip: Strategic Entry Points

Legendary investor Mark Mobius articulated what many institutional investors are thinking: "We've got to be prepared for a pullback. And you buy the dip." Historical data supports this approach—after the Nasdaq's first correction since 2010, it averaged 21.9% returns in the subsequent 12 months.

Value Opportunities Post-Correction:

-

DigitalOcean (DOCN): Cloud computing for SMBs, AI revenue doubled for five consecutive quarters

- Valuation: P/S ratio of 5.9 (29% discount to average 8.3 since IPO), P/E of 23.7 (vs. Nasdaq-100's 33.6)

- Price Targets: Bank of America and Canaccord raised to $60

-

Super Micro Computer (SMCI): Fell 60% during correction, yet fundamentals remain strong

- Growth Driver: Direct liquid cooling technology, rapid time-to-market for new AI tech

- Analyst Projection: 40% annual adjusted earnings growth through fiscal 2026

-

Meta Platforms (META): 17% slip during correction created entry point

- Undervaluation: Lower P/S than peers, 26% revenue growth, 43% operating margin

- AI Impact: Over $60 billion in AI-driven annual revenue

The OpenAI Wild Card: $1 Trillion Valuation?

One factor that could dramatically reshape the 2026 landscape: OpenAI's potential IPO.

The Setup:

- IPO Timeline: As early as late 2026, potentially extending to 2027

- Target Valuation: Up to $1 trillion (comparable to Apple, Microsoft, Nvidia, Alphabet)

- Capital Raise: At least $60 billion to fund AI infrastructure investments

- Current Metrics: $20 billion annualized revenue run rate, though mounting losses as infrastructure scales

Investment Implications:

- If successful, validates extreme AI valuations and could trigger another rally

- Secondary market already valued OpenAI at $500 billion (employees sold $6.6 billion in stock)

- Could create "halo effect" for AI pure-plays and enterprise partners

Risk Factors: The Bearish Case for 2026

No investment thesis is complete without acknowledging the risks:

Valuation Concerns

- 54% of institutional investors in October 2025 worried about an AI bubble

- Mobius warned of potential 30-40% pullback in AI stocks (though he'd "buy the dip aggressively")

- High earnings expectations may not materialize if competition intensifies

ROI Scrutiny Intensifies

- CFOs demanding measurable ROI within 6-12 months

- Current AI programs yielding ~16% ROI, projected to double by 2026 as implementations mature

- Projects failing to demonstrate tangible value will be discontinued

Energy and Infrastructure Bottlenecks

- U.S. data centers require additional 29 gigawatts of power by 2027

- Electricity demand from data centers could reach 6.7%-12% of total U.S. consumption by 2028 (up from 4.4% in 2023)

- Transmission capacity constraints, permitting delays, supply chain issues could slow growth

Regulatory Headwinds

- EU AI Act (effective August 2026) imposes stringent requirements for high-risk systems

- U.S. fragmented approach with state-level laws creating compliance complexity

- China's two-stage approach allowing innovation in pilots but requiring compliance at scale

Competition and Creative Destruction

- "CUDA lock-in" weakening as AMD ROCm, Google TPUs, and other alternatives mature

- Hyperscalers' custom silicon reducing dependence on Nvidia

- Agentic AI startups could disrupt established players with purpose-built solutions

Debt Financing Concerns

- Companies borrowed $75 billion in recent months for AI data centers (2x annual average)

- JPMorgan estimates $1.5 trillion in investment-grade bonds needed over next five years for data center build-out

- Rising interest rates could strain highly leveraged AI infrastructure projects

The Agentic AI Opportunity: 2026's Breakthrough Theme

While everyone focused on chips and infrastructure, the sleeper story of 2026 is agentic AI—autonomous agents that make decisions and execute tasks without constant human oversight.

Market Dynamics:

- 93% of IT leaders plan to introduce autonomous agents within two years

- 89% of CIOs consider agent-based AI a strategic priority

- 82% of enterprise leaders use generative AI weekly (up from 37% in 2023)

ROI Benchmarks:

- Cost Reduction: $1-4 saved per dollar spent, 80% lower Tier-1 support costs, 20-35% lower operational costs

- Productivity: 20-30% more output for same spend, 25%+ improvement in clinical/admin efficiency

- Revenue Growth: 10-30% increase in sales/conversions

Sector-Specific Opportunities:

- Healthcare: AI applications could generate $150 billion in annual savings by 2026

- Manufacturing: Global AI market reaching $230.95 billion by 2034 (44.20% CAGR)

- Supply Chain: 50% of solutions will use intelligent agents for autonomous decisions by 2030

- Financial Services: $97 billion projected investments by 2027

Regional Diversification: Beyond the Magnificent Seven

While U.S. mega-caps dominated AI investment in 2024-2025, 2026 presents opportunities for geographic diversification:

Emerging Markets Rally

- Weakening U.S. dollar, potential Fed rate cuts supporting EM bonds and equities

- 68% of global investors planning to diversify abroad, increasing allocations to:

- Europe: 30% (attractive valuations, moderate cyclical recovery expected)

- Asia-Pacific: 34% (China tech sector, India's digital infrastructure)

- Latin America: 22%

- Emerging Markets: 38%

China AI Opportunity

- Economy powered by trade and technology, AI playing significant role

- Equity market "deep, attractively priced, and under-owned by foreign investors"

- Expected growth above consensus, potentially reaching 5% in 2026

- Key Players: Baidu (AI search and autonomous driving), Alibaba Cloud, Tencent (gaming and social AI)

India's Digital Infrastructure Boom

- Favorable demographics, burgeoning digital infrastructure

- Role in diversifying global supply chains creating AI hardware opportunities

- Government AI pledge of $1.25 billion supporting ecosystem development

Europe's Recovery

- GDP growth expected at 1-1.5% in 2026, moderate but steady

- Equities more attractively priced than U.S. counterparts

- Broader, more diversified investment opportunities beyond tech concentration

Investment Strategies for 2026: Three Playbooks

The Aggressive Growth Playbook

For investors with high risk tolerance and long time horizons:

- Core Holdings (60%): Nvidia, AMD, Microsoft—benefiting from infrastructure spending surge

- Growth Bets (25%): SoundHound AI, Tempus AI, Super Micro Computer—high-growth pure-plays

- Wildcards (15%): Pre-IPO OpenAI exposure via secondary markets, early agentic AI startups

Rationale: Maximum exposure to AI's exponential growth phase, accepting high volatility

The Balanced Value Playbook

For investors seeking exposure with downside protection:

- Undervalued Giants (50%): Meta, Alphabet—AI monetization with reasonable valuations

- Infrastructure REITs (20%): Digital Realty, Equinix—benefiting from data center demand with dividend income

- Diversified Tech (20%): ServiceNow, Salesforce—enterprise AI adoption with established customer bases

- Emerging Markets (10%): China/India AI exposure via ETFs

Rationale: AI exposure without extreme valuations, income generation, geographic diversification

The Income-Focused Playbook

For conservative investors seeking AI exposure with capital preservation:

- High-Quality Bonds (50%): Investment-grade corporate bonds from Microsoft, Apple funding AI infrastructure

- Dividend Aristocrats with AI Initiatives (30%): Traditional companies leveraging AI for efficiency (IBM, Cisco)

- AI-Adjacent REITs (15%): Data center REITs providing infrastructure without direct tech exposure

- Cash Reserves (5%): Dry powder for opportunistic "buy the dip" moments

Rationale: Capital preservation while benefiting from AI's infrastructure buildout and steady income

The 2026 Bottom Line: Cautious Optimism Wins

After the turbulence of 2025, Wall Street's 2026 outlook can be summarized in three words: cautiously, strategically bullish.

The correction wasn't a death sentence for AI—it was a necessary reset that separated genuine innovation from speculative froth. The companies that survived with strong fundamentals, clear monetization paths, and disciplined capital allocation are now positioned for sustained growth.

Key takeaways for investors:

- Infrastructure spending isn't slowing—Big Tech's $405 billion+ capex proves commitment to AI's long-term potential

- The monetization wave is here—Agentic AI delivering 5x-10x ROI demonstrates tangible value creation

- Competition benefits investors—AMD, Intel, custom silicon challenging Nvidia creates better pricing, innovation

- Valuations matter again—Meta, Alphabet, DigitalOcean offer compelling entry points with lower multiples

- Diversification is essential—Geographic spread and subsector allocation reduce concentration risk

- Regulation is clarifying, not killing—Clear frameworks (EU AI Act, etc.) provide operational certainty

- Energy constraints are solvable—Liquid cooling, edge computing, efficiency gains addressing infrastructure strain

The $800 billion correction of 2025 wasn't the end of the AI revolution—it was the beginning of its maturation. And for investors willing to look past the volatility, 2026 presents the most compelling risk-reward setup since the early cloud computing days.

As Mark Mobius said: "We've got to be prepared for a pullback. And you buy the dip." The dip happened. Now it's time to buy strategically.

References and Data Sources

- Bank of America institutional investor survey (October 2025) - 80% expect 2026 market pullback

- Goldman Sachs Research - $720 billion grid infrastructure spending through 2030

- Gartner forecasts - AI-optimized IaaS exceeding $37.5 billion in 2026

- Grand View Research - AI agents market reaching $50.31 billion by 2030

- FTI Consulting - AI investment landscape analysis

- S&P Global Commodity Insights - Data center power demand projections

- U.S. Department of Energy - Data center electricity consumption forecasts

- Wall Street analyst consensus (Bank of America, Canaccord Genuity, KeyBanc, Goldman Sachs)

- Company earnings reports and guidance (Meta, Microsoft, Alphabet, AMD, Nvidia, OpenAI)

- McKinsey & Company - Agentic AI productivity analysis and ROI benchmarks

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Markets and competitive dynamics can change rapidly in the technology sector. Taggart is not a licensed financial advisor and does not claim to provide professional financial guidance. Readers should conduct their own research and consult with qualified financial professionals before making investment decisions.

Taggart Buie

Writer, Analyst, and Researcher