The Great AI Unraveling: Why Wall Street Had Its Worst Week Since the Pandemic

Despite Nvidia's record earnings, the AI trade experienced its most dramatic sell-off in years. Ray Dalio warns of a bubble, Michael Burry shorts the sector, and a new metaphor captures the terrifying truth: AI infrastructure might be 'digital lettuce'—perishable goods with expiration dates nobody wants to admit.

The Great AI Unraveling: Why Wall Street Had Its Worst Week Since the Pandemic

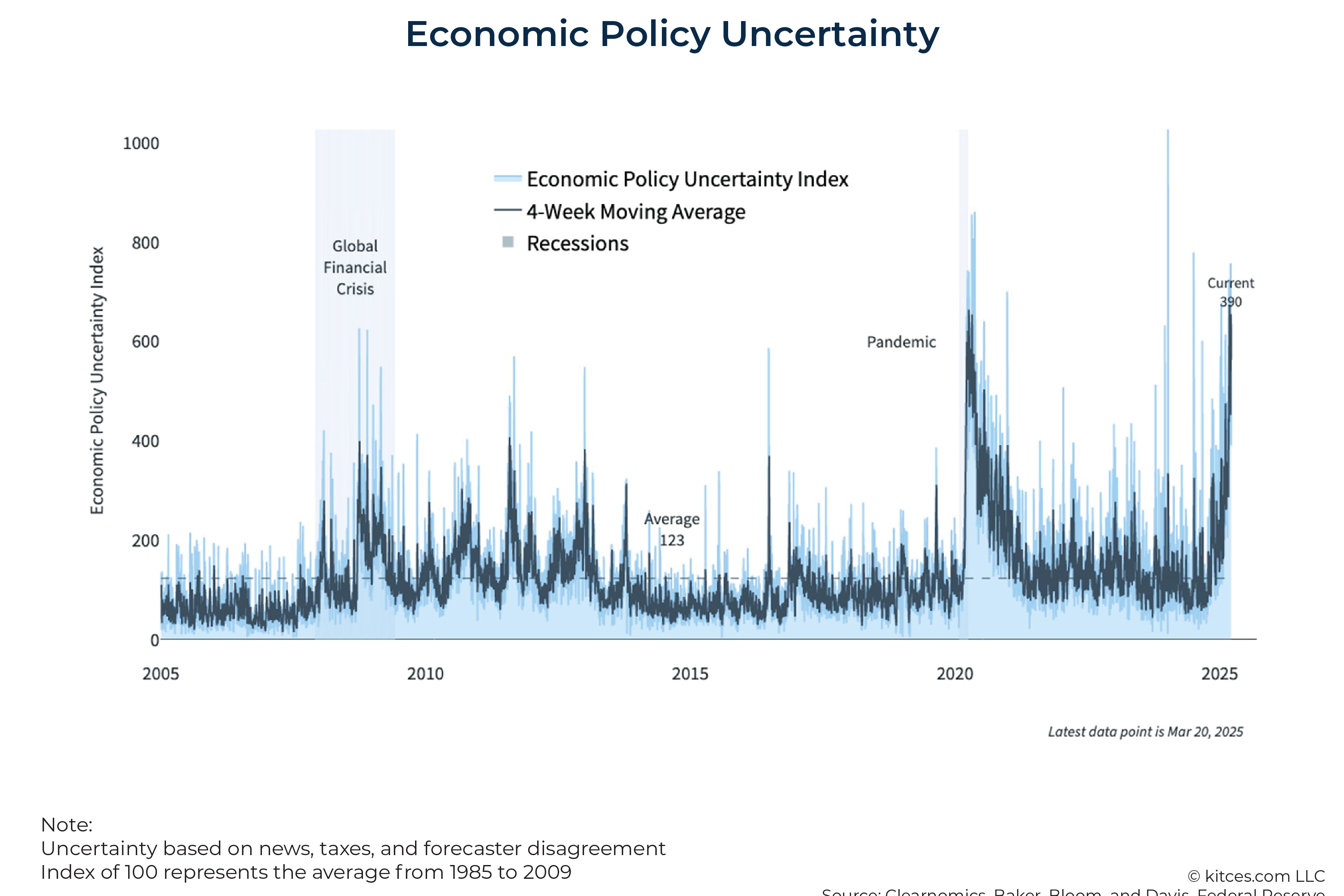

The week of November 18-22, 2025, will be remembered as the moment the AI investment thesis cracked. Despite Nvidia posting blowout earnings that exceeded every Wall Street estimate, tech stocks experienced their worst week since the pandemic-era volatility of early 2020. The S&P 500 shed 3.2% for the week, the Nasdaq plunged 4.8%, and even Bitcoin—the ultimate risk-on asset—cratered below its April lows, heading for its worst monthly performance since the 2022 crypto collapse.

But the numbers only tell part of the story. What made this week extraordinary wasn't just the magnitude of the losses—it was who was sounding the alarm and how they described what's happening. From Ray Dalio's blunt "we're definitely in a bubble" to economist David McWilliams' haunting metaphor of AI hardware as "digital lettuce," the narrative around artificial intelligence investments fundamentally shifted from "how much will we make?" to "when does this end badly?"

The "Digital Lettuce" Metaphor That Captured Wall Street's Anxiety

Of all the analysis produced during this turbulent week, nothing captured the emerging consensus quite like David McWilliams' description of AI infrastructure as "digital lettuce." In an interview that went viral among fund managers, the Irish economist argued that massive AI data centers—those gleaming temples to computational power that companies like Oracle, Microsoft, and Meta are building for tens of billions of dollars—are essentially perishable goods.

"Think about it," McWilliams explained. "You buy lettuce, it starts degrading immediately. You have a narrow window to use it before it becomes worthless. AI chips and data centers work the same way. The hardware you buy today will be obsolete in 18-24 months because the next generation will be 10x faster, more efficient, and cheaper to operate. These aren't long-term assets—they're consumables dressed up as infrastructure."

The metaphor struck a nerve because it articulates what many investors are beginning to suspect: the AI boom is fundamentally different from previous technology cycles. When companies built railroads in the 1800s or telecommunications networks in the 1990s, that infrastructure maintained value for decades. The tracks laid in 1890 still carried trains in 1990. But AI infrastructure faces technological obsolescence on a scale and speed that makes traditional depreciation schedules look absurdly optimistic.

This matters enormously because of how companies account for these investments. When Nvidia sells $100 billion worth of H100 and Blackwell chips, the buyers (Microsoft, Meta, Oracle, etc.) don't expense that cost immediately. They depreciate it over 5-7 years, spreading the cost across many quarters. This makes their earnings look strong and their spending sustainable.

But what if those chips are effectively worthless after three years? Suddenly, companies are dramatically understating their true costs, overstating their profits, and misleading investors about the economics of their AI buildouts. Michael Burry—the investor immortalized in "The Big Short" for predicting the 2008 housing crisis—made exactly this argument this week when he revealed substantial short positions against Nvidia and Palantir, accusing hyperscalers of "understating depreciation expenses for chips."

Ray Dalio: "We're Definitely in a Bubble"

Ray Dalio doesn't make proclamations lightly. The 76-year-old founder of Bridgewater Associates—the world's largest hedge fund with $221 billion under management—built his reputation on rigorous analysis and contrarian insights. So when Dalio stated flatly on November 20th that "we're definitely in a bubble," markets took notice.

Dalio's concern centers on valuation extremes and capital misallocation. He noted that the "Magnificent Seven" tech companies (Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia, and Tesla) now represent 32% of the S&P 500's total market capitalization—the highest concentration since the dot-com peak in March 2000. "Whenever you see this kind of concentration," Dalio warned, "it means capital is flooding into a narrow set of bets, often for reasons that don't hold up under scrutiny."

The numbers support his concern:

- Nvidia trades at 48x forward earnings despite growth expected to decelerate sharply as comps get harder

- Microsoft's Azure AI revenue must grow 60% annually for the next four years just to justify its current stock price

- Meta trades at a 40% premium to the broader market despite announcing it will double AI infrastructure spending in 2026 to over $100 billion

- Oracle's stock fell 11% this week despite announcing $50 billion in new AI data center projects—because investors are increasingly worried about the $104 billion in total debt the company has accumulated to fund these bets

"The market is pricing in perfection," Dalio observed. "AI needs to not just succeed—it needs to succeed ahead of schedule and above expectations for current valuations to make sense. History suggests that almost never happens."

Sundar Pichai's Surprising Admission: "Elements of Irrationality"

Perhaps the most striking moment of the week came from an unexpected source: Sundar Pichai, CEO of Alphabet (Google's parent company). Speaking at a technology conference on November 21st, Pichai acknowledged "elements of irrationality" in current AI investment behavior, explicitly comparing the current environment to the dot-com bubble of 1999-2000.

"I lived through the dot-com era," Pichai said. "There are similarities in the exuberance, the capital flows, and the disconnect between near-term fundamentals and long-term expectations. Not every AI company will survive. Not every investment will pay off. And no company—including Google—would be immune if this bubble bursts."

The admission was remarkable both for its candor and its source. Pichai isn't a bearish analyst or a short-seller with an agenda—he's the CEO of one of AI's biggest winners, a company that gained 8% this week (the only member of the Magnificent Seven to post gains) on enthusiasm for its new Gemini 3 model. For Pichai to acknowledge bubble dynamics suggests the concerns have spread even to AI's leadership class.

The Nvidia Paradox: Record Earnings, Falling Stock

Wednesday, November 20th should have been Nvidia's coronation. The AI chip giant reported third-quarter results that demolished expectations:

- Revenue: $44.6 billion (up 110% year-over-year, $2.8 billion above estimates)

- Net income: $23.4 billion (up 65%, margin expansion of 300 basis points)

- Data center revenue: $38.9 billion (up 127%, with Blackwell chips just beginning to ship)

- Guidance: Q4 revenue of $46.5 billion (above the $43.2 billion consensus)

CEO Jensen Huang proclaimed that demand for Blackwell systems was "off the charts" and production would triple in Q1 2026. Every metric screamed "buy."

Instead, Nvidia's stock fell 3.6% on the day and ended the week down 8.2%. Other chip stocks fared even worse: AMD dropped 16%, Micron fell 14%, and Oracle cratered 11%. The Nasdaq posted one of its worst single-day performances of the year.

What happened? Investors finally asked the question they'd been avoiding: What happens when the music stops?

Nvidia's business model depends on a continuous cycle of upgrades. Customers buy H100 chips, then 18 months later buy Blackwell chips because they're better, then 18 months after that buy the next generation. This works beautifully during a buildout phase when companies are racing to deploy AI capabilities and nobody wants to fall behind.

But it creates two problems:

First, revenue becomes lumpy and unpredictable. If customers decide to skip a generation or delay purchases by six months, Nvidia's growth rate could collapse overnight. The company is essentially selling to ~20 large customers (the hyperscalers and major cloud providers), which means revenue concentration risk is extreme.

Second, customer economics have to work. If Microsoft, Meta, and Amazon invest $500 billion in AI infrastructure over the next two years and don't generate sufficient revenue to justify those investments, they'll stop buying—and Nvidia's business model breaks.

This week, investors began seriously contemplating both scenarios.

The Bond Market's $90 Billion Warning Signal

While equity markets grabbed headlines, an equally important story unfolded in corporate bond markets. Since September, major tech companies have issued nearly $90 billion in bonds, with expectations that 2025's total issuance will exceed $120 billion—the highest annual figure on record.

The debt spree includes:

- Alphabet: $25 billion in bonds issued October 2025

- Meta: $15 billion issued in August-September 2025

- Oracle: $18 billion issued November 2025

- Amazon: $12 billion issued September 2025

On the surface, these offerings make sense. With investment-grade ratings and interest rates declining from 2023-2024 peaks, these companies can borrow cheaply. But the use of proceeds reveals the underlying tension: a significant portion is earmarked specifically for AI infrastructure.

Oracle's $18 billion bond sale is particularly instructive. The company plans to spend $38 billion on AI data centers over the next three years—funded partly by debt, partly by cash flow. But Oracle already carries $104 billion in total debt (including operating leases), giving it one of the highest debt-to-EBITDA ratios among large tech companies at 3.2x.

Credit markets are beginning to price in risk. Oracle's bonds trade at a spread of 110 basis points over Treasuries—not distressed territory, but meaningfully wider than peers like Microsoft (40 bps) or Apple (35 bps). Bond investors are essentially saying: "We'll lend to Oracle, but we want extra yield because this AI buildout carries real risk of not paying off."

The concern echoes throughout credit markets. Fund managers surveyed by Bank of America in mid-November reported that a majority of their clients believe companies are overspending on AI infrastructure. One credit analyst told Reuters: "We're financing a gold rush where nobody's found gold yet. Eventually, somebody has to show me the revenue."

The Depreciation Time Bomb

Michael Burry's revelation that he's shorting Nvidia and Palantir brought mainstream attention to an issue that accounting nerds have been debating for months: AI hardware depreciation schedules.

Here's the technical issue: when companies buy AI chips and build data centers, they capitalize those costs as long-term assets and depreciate them over their "useful life." Most companies assume 5-7 years for servers and 7-10 years for data center infrastructure.

But Burry argues—and an increasing number of analysts agree—that AI hardware has a much shorter useful life due to rapid technological advancement. If your competitor deploys next-generation chips that train models 10x faster and run inference 5x cheaper, your 18-month-old infrastructure isn't just less valuable—it's potentially worthless because you can't compete economically.

The implications are staggering. If companies need to depreciate AI hardware over 3 years instead of 7, their annual depreciation expenses roughly double. This would:

- Reduce reported earnings for Microsoft, Meta, Amazon, and Google by an estimated $30-40 billion annually

- Make many AI projects unprofitable on a cash-return basis

- Reveal that the "amazing" margins companies are reporting on AI services are actually quite thin or negative

Jensen Huang pushed back hard against this narrative, arguing that Nvidia's CUDA software platform and the cumulative performance improvements in GPU architectures mean "our chips have a useful life of 5-6 years, not 2-3." But this claim is difficult to verify, and Burry's track record of spotting accounting irregularities gives his skepticism weight.

What Happens Next?

The AI market stands at an inflection point. For the past three years, the investment thesis has been simple: AI is revolutionary, early movers will dominate, and you can't afford to be left behind. This narrative drove valuations to stratospheric levels and justified almost unlimited capital expenditures.

This week cracked that consensus. Not because AI isn't revolutionary—it almost certainly is—but because investors are finally asking hard questions about timing, economics, and who captures the value.

Several scenarios could play out:

Scenario 1: The "Soft Landing"

AI revenue growth accelerates dramatically in 2026-2027, validating current investments. Microsoft, Google, and others successfully monetize their AI capabilities at enterprise scale, generating returns that justify infrastructure spending. Nvidia maintains its technology lead and pricing power. In this scenario, the current volatility is just a healthy correction in an ongoing bull market.

Scenario 2: The "Long Winter"

AI delivers on its promise, but monetization takes 5-7 years longer than expected. Companies are forced to write down investments, cut AI spending, and refocus on profitable core businesses. Nvidia faces a multi-year revenue drought as customers digest existing capacity. Stock prices decline 40-60% from peaks but eventually recover as AI economics improve. This is the dot-com analog: painful but not catastrophic.

Scenario 3: The "Digital Lettuce Collapse"

Rapid technological advancement makes current AI infrastructure obsolete faster than depreciation schedules assume. Companies are forced to take massive write-downs. Credit markets seize up as debt-funded AI buildouts collapse. A wave of AI startups fails, and even larger players sharply curtail spending. Stock prices decline 70-80%. This is the true bubble-burst scenario.

Which scenario unfolds depends largely on factors we won't know for 12-24 months: enterprise AI adoption rates, the pace of technological advancement, and whether companies can actually generate revenue that justifies their infrastructure investments.

The Investment Implications

For investors trying to navigate this uncertainty, several principles emerge:

1. Differentiate between AI winners and AI spenders.

Nvidia, with 80%+ gross margins and minimal capital intensity, is fundamentally different from Oracle, which is borrowing billions to build data centers. Even in a downturn, Nvidia cuts prices and survives. Oracle might face existential balance sheet stress.

2. Watch the bond market, not the stock market.

Equity investors are optimistic by nature. Bond investors are ruthless accountants. If credit spreads for tech companies continue widening, that's a canary in the coal mine that default risks are rising.

3. Revenue, not capability, is what matters.

AI demonstrations are impressive, but companies need to show they can charge customers enough to cover infrastructure costs plus a return on investment. Until we see sustained AI-driven revenue growth at scale, skepticism is warranted.

4. Diversify beyond AI.

The market's 32% concentration in the Magnificent Seven represents huge single-factor risk. If the AI trade unwinds, broad indexes will suffer, but non-AI sectors could hold up or even benefit as capital flows elsewhere.

Conclusion: The Reckoning Begins

This week may not mark the peak of the AI bubble—bubbles can inflate far longer than rational analysis suggests they should. But it does mark the moment when the bull case shifted from "obviously true" to "hotly debated." When Ray Dalio calls it a bubble, when Sundar Pichai acknowledges irrationality, when Michael Burry shorts the sector, and when Nvidia's blowout earnings fall flat, something fundamental has changed.

The "digital lettuce" metaphor captures a truth that investors are only beginning to grapple with: AI infrastructure may not be the durable, value-preserving asset that accounting conventions assume. If technological progress continues at its current breakneck pace, today's cutting-edge data center could be tomorrow's expensive liability.

For three years, the AI trade has been driven by FOMO—the fear of missing out. This week, a new fear emerged: the fear of being the last buyer at the top. In markets, that shift in psychology is often the most important signal of all.

Market data as of November 22, 2025. This article is for informational purposes only and should not be considered investment advice.

Sources & References

- 1. CNBC Market Coverage - "S&P 500 and Nasdaq Post Biggest Weekly Losses in Months Amid Tech Sell-Off" - November 18-22, 2025

- 2. Futurism - David McWilliams Interview: "AI Investments Are 'Digital Lettuce' That Will Crash" - November 21, 2025

- 3. CNBC - Ray Dalio Comments on Market Bubble Conditions - November 20, 2025

- 4. BBC News - Sundar Pichai Conference Remarks on AI Irrationality - November 21, 2025

- 5. Nvidia Corporation - Q3 FY2026 Earnings Report and Conference Call - November 20, 2025

- 6. U.S. Securities and Exchange Commission - Michael Burry 13F Filing Disclosure - November 2025

- 7. Bank of America - Global Fund Manager Survey Results - November 2025

- 8. Reuters - "Tech Companies Issue $90 Billion in Bonds to Fund AI Infrastructure" - November 21, 2025

- 9. Oracle Corporation - Bond Offering Documents and Use of Proceeds - November 2025

- 10. Fortune Magazine - "Big Tech's AI Spending Spree: Who Will Benefit?" - November 2025

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Markets and competitive dynamics can change rapidly in the technology sector. Taggart is not a licensed financial advisor and does not claim to provide professional financial guidance. Readers should conduct their own research and consult with qualified financial professionals before making investment decisions.

Taggart Buie

Writer, Analyst, and Researcher