OpenAI's Code Red: Inside the $8.65 Billion Crisis That Has Sam Altman Scrambling

How the AI golden child went from $500B darling to crisis mode in 60 days. Leaked documents reveal OpenAI spent $8.65 billion on inference while generating only $4.33 billion in revenue, as Google's Gemini 3 and Anthropic's Claude capture market share and partners accumulate $100 billion in debt.

OpenAI's Code Red: Inside the $8.65 Billion Crisis That Has Sam Altman Scrambling

How the AI golden child went from $500B darling to crisis mode in 60 days—and what it means for the entire industry

By Taggart Buie

December 8, 2025

18 min read

After three years of using ChatGPT daily, Salesforce CEO Marc Benioff made a stunning announcement in November 2025: he was switching to Google's Gemini 3. "The leap is insane," he declared on social media. "The world just changed, again."

For OpenAI, it wasn't just the world that was changing—it was collapsing.

Within days of Benioff's defection, leaked documents revealed a financial reality starkly at odds with CEO Sam Altman's public optimism. While Altman claimed OpenAI was on track for a $20 billion annualized revenue run rate, internal Microsoft payment records suggested actual quarterly revenue of just $4.33 billion for the first nine months of 2025—barely more than a quarter of the claimed figure.

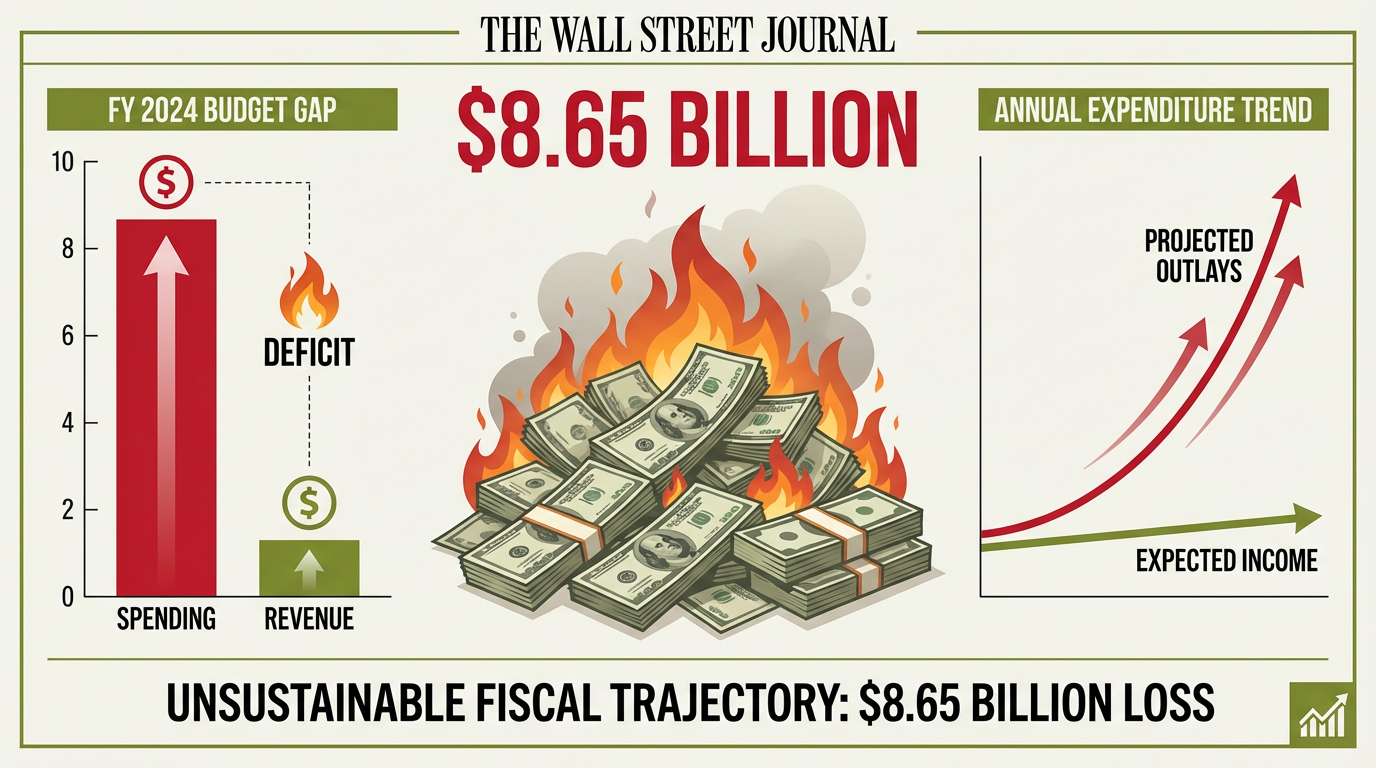

Even more alarming: OpenAI spent $8.65 billion on inference costs alone during that same period. The company wasn't just missing revenue targets—it was losing money on every query.

The response was swift and dramatic. In early December, Altman issued an internal "code red" memo to staff, cancelling planned expansions into advertising, shopping, and healthcare to refocus entirely on ChatGPT's core functionality. Marketing campaigns were scrapped. Product launches were delayed. The company that had seemed unstoppable just months ago was in full retreat.

What's driving this crisis? A perfect storm of competitive pressure, unsustainable spending, and mounting evidence that the emperor—valued at $500 billion—might have no clothes.

The Revenue Mirage: When the Math Doesn't Add Up

Let's start with the numbers that don't make sense.

Sam Altman has consistently painted a picture of explosive growth. In June 2025, he announced OpenAI had reached a $10 billion annualized run rate. By July, that figure had jumped to $12 billion. In August, he told investors revenue was "well more" than $13 billion annually. By year's end, analysts expected OpenAI to hit $15-20 billion.

But leaked financial documents tell a different story.

According to internal Microsoft records obtained by TechCrunch, OpenAI paid its primary partner $865.8 million in revenue share during the first nine months of 2025—up from $493.8 million in all of 2024. Under the terms of their partnership, Microsoft receives approximately 20% of OpenAI's revenue after covering its Azure compute costs.

Do the math: if Microsoft received $865.8 million for nine months of revenue sharing, that implies OpenAI generated approximately $4.33 billion in actual revenue during the first nine months of 2025. Annualized, that's roughly $5.8 billion—less than half of Altman's claimed $12-13 billion figure, and nowhere close to the $20 billion run rate projected for year-end.

How can there be such a massive discrepancy? The answer appears to lie in how "annualized run rate" is calculated. Rather than actual cash revenue over 12 months, OpenAI likely takes its single best month—say, October 2025—and multiplies by 12. If October generated $1.5 billion in bookings (perhaps including multi-year enterprise contracts signed that month), suddenly you have an "$18 billion ARR."

It's technically accurate. It's also deeply misleading.

"This is the kind of accounting gymnastics that would make Enron blush," says Gary Smith, an economics professor at Pomona College who has studied OpenAI's financial disclosures. "When your claimed revenue is three to four times your actual cash coming in the door, you're not building a business—you're building a house of cards."

The implications are staggering. If OpenAI is only generating $5-6 billion in actual annual revenue, the company's $500 billion valuation represents a price-to-sales ratio of nearly 100x. Even in the frothy world of tech unicorns, that's stratospheric. Apple, the world's most valuable company, trades at less than 9x sales.

The Inference Cost Crisis: Spending $8.65 Billion to Make $4.33 Billion

But inflated revenue projections are only half the problem. The real crisis is on the cost side.

Those same leaked Microsoft documents reveal that OpenAI spent $8.65 billion on inference costs—the compute resources required to generate responses to user queries—during just the first nine months of 2025. That's up from $3.8 billion for all of 2024, representing a 127% increase in less than a year.

Let that sink in: OpenAI spent $8.65 billion on inference while generating approximately $4.33 billion in revenue during the same period. The company was losing roughly $2 for every $1 it brought in, before accounting for research and development, employee salaries, or any other operational expenses.

According to financial analysts who reviewed Microsoft's Q3 2025 disclosures, OpenAI recorded operating losses of $12 billion in that quarter alone. For the first half of 2025, R&D spending reached $6.7 billion on top of the $5.02 billion in inference costs.

The total 2025 cash burn? Approximately $8 billion, with some industry watchers projecting it could reach $45 billion annually by 2028 if current trajectories continue.

"Every time someone uses ChatGPT, OpenAI loses money," explains Ben Inker, co-head of asset allocation at investment firm GMO. "That's not a business model—that's a charity operation funded by the world's most expensive venture capital round."

When might OpenAI become profitable? According to internal forecasts obtained by Fortune, the company won't achieve positive cash flow until 2029 or 2030—and that's assuming everything goes right. To hit that target, OpenAI would need to reach approximately $200 billion in annual revenue by 2030 while simultaneously cutting inference costs per query by 90%.

For context, Alphabet (Google's parent company) generated $307 billion in revenue in 2024 after 26 years in business. OpenAI would need to achieve two-thirds of Google's revenue in less than a decade, while fundamentally transforming its cost structure.

Scott Galloway, a tech analyst and professor at NYU's Stern School of Business, is blunt in his assessment: "OpenAI is a trainwreck from a financial management perspective. They're spending more than double their estimated $13 billion in annual revenue, and there's no clear path to profitability. If this company collapses, there will be nowhere to hide for investors."

Code Red: The Strategic Retreat Nobody Saw Coming

The December 2025 "code red" memo marked a stunning reversal for a company that had seemed poised for limitless expansion.

According to sources who reviewed the internal communication, Altman ordered an immediate halt to several high-profile initiatives:

Advertising integration: Despite leaked Android app code revealing plans for "sponsored" content, "search ads," and a "bazaar" marketplace, all advertising features were postponed indefinitely. The potential revenue stream—estimated at $2-3 billion annually by some analysts—was sacrificed to preserve ChatGPT's user experience.

AI shopping assistants: A planned feature that would help users research products and complete purchases was shelved, eliminating another potential revenue source just as the holiday shopping season ramped up.

Health agents: OpenAI had been quietly developing AI tools for medical diagnosis and health management, with pilot programs at several hospital systems. All were put on hold pending "further research."

Pulse personal assistant: An ambitious upgrade to make ChatGPT more proactive—automatically scheduling meetings, sending reminders, and anticipating user needs—was delayed until at least mid-2026.

Instead, Nick Turley, OpenAI's head of ChatGPT, said the company would focus on making the chatbot "even more capable, growing its user base, and expanding access across the globe" while making it "even more intuitive and personal."

Translation: we're losing ground to Google, and we need to get back to basics before it's too late.

The timing is no coincidence. In the months leading up to Altman's memo, Google's Gemini 3 had gone from distant also-ran to genuine threat. Monthly active users surged from 450 million in July to 650 million by October—adding 200 million users in just three months. Meanwhile, user engagement data showed people were spending more time with Gemini than ChatGPT, a metric that once seemed unthinkable.

Even more concerning: the defections were coming from the top. Beyond Marc Benioff, several Fortune 500 CTOs have quietly shifted their organizations from OpenAI to either Google or Anthropic, citing better performance, lower costs, and more reliable service.

"The enterprise market is where the real money is, and OpenAI is losing it," says a senior AI researcher at a major tech company who spoke on condition of anonymity. "When the CEO of Salesforce—one of the most influential voices in enterprise software—publicly abandons your product, that's not a competitive threat. That's an existential crisis."

Altman's response? Fast-track a new large language model codenamed "Garlic"—potentially GPT-5.2 or GPT-5.5—specifically designed to counter Google's coding and reasoning advantages. The rush is so urgent that OpenAI reallocated engineering resources from other projects, causing additional delays across the product roadmap.

It's the kind of reactive, panic-driven decision-making that raises questions about whether OpenAI ever had a sustainable long-term strategy, or whether the company has simply been making it up as it goes along.

The Google Threat: When 650 Million Users Tell a Story

To understand why Altman declared code red, you need to understand just how dramatically Google's Gemini 3 has outperformed expectations.

Launched in mid-November 2025, Gemini 3 didn't just match GPT-5.1—it dominated it across nearly every meaningful benchmark:

Humanity's Last Exam: Gemini 3 scored 1324 versus GPT-5.1's 1220, a gap of 104 points on a test designed to be beyond the capability of current AI systems.

GPQA Diamond (graduate-level science questions): 91.9% accuracy for Gemini 3 versus 88.1% for GPT-5.1, with Gemini reaching 93.8% when allowed to "think" through problems.

ARC-AGI-2 (abstract reasoning): Gemini 3 scored 31.1% (45.1% with extended thinking) compared to GPT-5.1's 17.6%—a 76% performance advantage.

LiveCodeBench Pro (real-world coding): Gemini 3 achieved an Elo rating of 2,439 versus GPT-5.1's 2,243, nearly 200 points higher. In chess terms, that's the difference between a grandmaster and a strong amateur.

SWE-Bench Verified (software bug fixing): Gemini 3 solved 76.2% of real-world GitHub issues, competitive with the market-leading Claude Opus 4.5 at 77.2%, and significantly ahead of GPT-5.1.

But benchmarks only tell part of the story. The real threat is Google's distribution advantage.

Gemini 3 is integrated into Google Search, which handles 8.5 billion queries daily. It's in Gmail, Google Docs, Google Maps, YouTube, and Android devices. By conservative estimates, Gemini has access to 1-5 billion devices worldwide—a distribution network that would take OpenAI decades to build, if it ever could.

Within 24 hours of Gemini 3's launch, more than 1 million developers had accessed it through Google AI Studio and the Gemini API. The AI Overview feature in Google Search—which uses Gemini to generate summaries for complex queries—reached 1.5 billion monthly users. All of this while ChatGPT's user growth appeared to be plateauing.

Perhaps most damaging was the Salesforce defection. Marc Benioff is no ordinary user—he's one of the most influential voices in enterprise software, with deep relationships across Fortune 500 boardrooms. His public endorsement of Gemini 3 as "sharper and faster" with "insane" improvements in reasoning and processing carried more weight than a hundred benchmark scores.

"When you lose the enterprise market, you lose the profit margin," explains a former OpenAI business development executive. "Consumers might use ChatGPT for free, but enterprises pay $25-60 per user per month. That's where you make your money. And right now, Google and Anthropic are eating OpenAI's lunch."

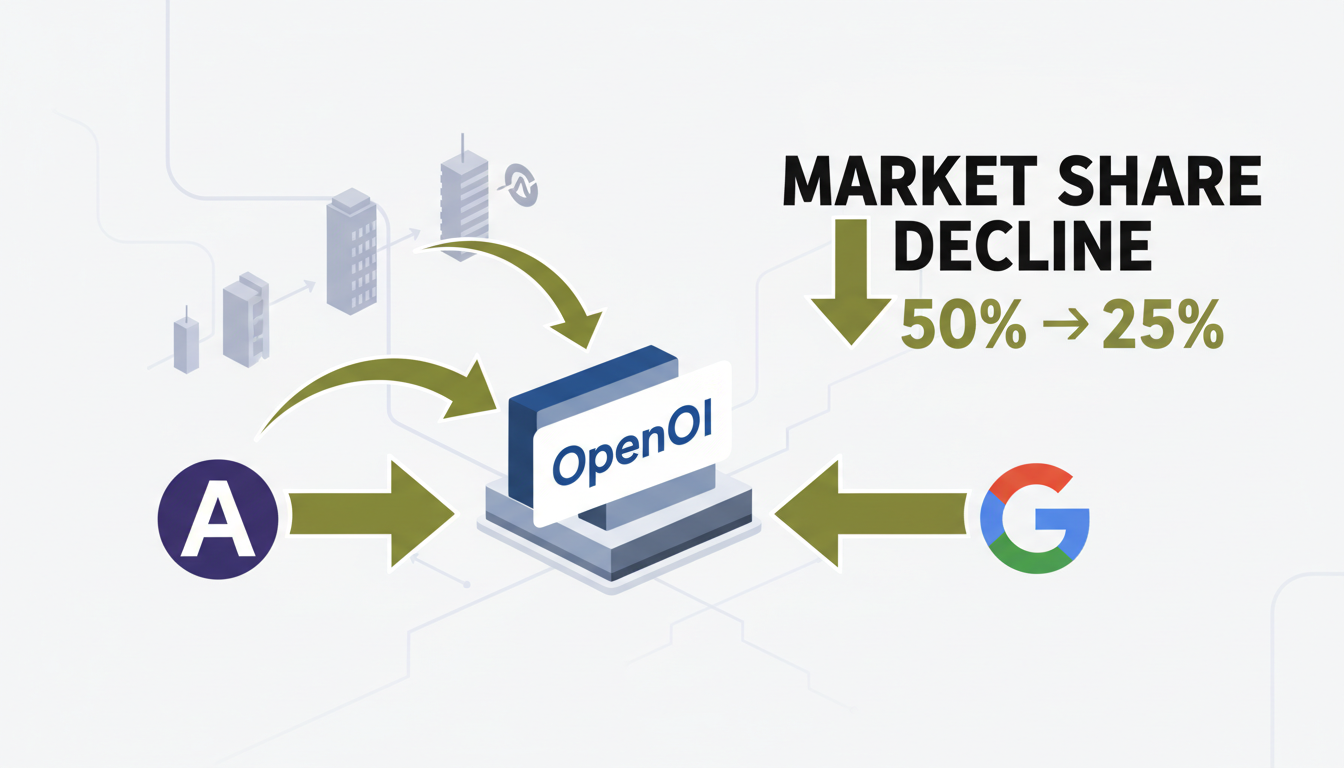

The market share data confirms it. According to a July 2025 survey by Menlo Ventures, Anthropic's Claude captured 32% of the enterprise AI market, compared to OpenAI's 25% and Google's 20%. Among enterprise coding workloads specifically, Claude dominated with 42% share versus OpenAI's 21%.

This represents a stunning reversal from just two years ago, when OpenAI held an estimated 50% of the enterprise market while Anthropic had barely 12%. The trend line is clear—and it's pointing in the wrong direction.

The $1.15 Trillion Infrastructure Trap

If OpenAI's operating costs and competitive position weren't concerning enough, there's the matter of $1.15 trillion in infrastructure commitments that will come due over the next decade.

Yes, trillion with a T.

Since 2024, OpenAI has signed a series of agreements to secure the massive computational resources needed to train future AI models and serve billions of user queries:

- Microsoft Azure: $250 billion for cloud computing services

- Oracle: $300 billion over five years (2027-2031), with $60 billion annually in the peak years

- Amazon AWS: $38 billion over seven years

- CoreWeave: $22.4 billion for data center usage rights through 2029

- Broadcom: $350 billion for custom AI accelerators (2026-2032)

- Nvidia: $100 billion investment in exchange for non-voting shares and data center capacity

- AMD: $90 billion for Instinct GPUs plus warrants for 160 million AMD shares

The total: $1.15 trillion committed through 2035, with annual spending projected to hit $6 billion in 2025, $14 billion in 2026, and $50 billion by 2027.

To put that in perspective: OpenAI has committed to spending 70 times its actual 2025 revenue over the next decade. Even if the company achieves its optimistic $100 billion revenue target by 2027, these infrastructure commitments would represent 14 times annual revenue—a level of leverage that would make even the most aggressive tech companies pause.

The individual deals are equally eye-popping. Oracle's $300 billion commitment represents roughly 15 times the company's annual revenue. Since announcing the deal, Oracle's stock has lost $315 billion in market value—more than the entire contract is worth—as investors questioned the wisdom of betting the company's future on OpenAI's success.

But here's the truly dangerous part: OpenAI isn't paying for most of this itself. The company's partners are.

According to reporting by the Times of India and Data Center Dynamics, OpenAI's partners have accumulated nearly $100 billion in debt to finance these infrastructure buildouts:

- SoftBank, Oracle, and CoreWeave have borrowed $30 billion+

- Blue Owl and Crusoe Energy secured $28 billion in additional loans

- Banks are arranging another $38 billion in financing for Oracle and Vantage Data Centers

Meanwhile, OpenAI maintains a $4 billion credit facility that remains largely untouched. The company has effectively transferred the financial risk of its massive infrastructure needs to partners and lenders, while retaining control of the resulting capacity.

"It's brilliant, in a terrifying sort of way," says Paul Kedrosky, a venture capitalist and research fellow at MIT. "OpenAI gets access to $1.15 trillion in infrastructure without taking on the debt themselves. But if the revenue doesn't materialize, it's not OpenAI that collapses—it's Oracle, CoreWeave, and a dozen other companies that have bet everything on Sam Altman's vision."

Some analysts go further, suggesting the entire structure resembles a house of cards propped up by circular financing. Nvidia invests $100 billion in OpenAI, which then uses that capital to buy Nvidia chips. OpenAI exchanges equity in exchange for CoreWeave data center capacity, then uses that stock to pay rent. Each deal creates the appearance of booming demand, justifying the next round of investment.

"At some point, someone needs to ask: where does the actual money come from?" Kedrosky adds. "Because right now, it looks like everyone is using everyone else's money to create the illusion of a viable business."

Microsoft's Stranglehold: The October Agreement Nobody Noticed

In late October 2025, as the tech world focused on product launches and earnings reports, OpenAI and Microsoft quietly signed a new agreement that fundamentally reshaped their relationship.

The headlines emphasized partnership and collaboration. But buried in the details was something more concerning: Microsoft had tightened its grip on OpenAI in ways that might prove difficult—or impossible—to escape.

Under the new agreement:

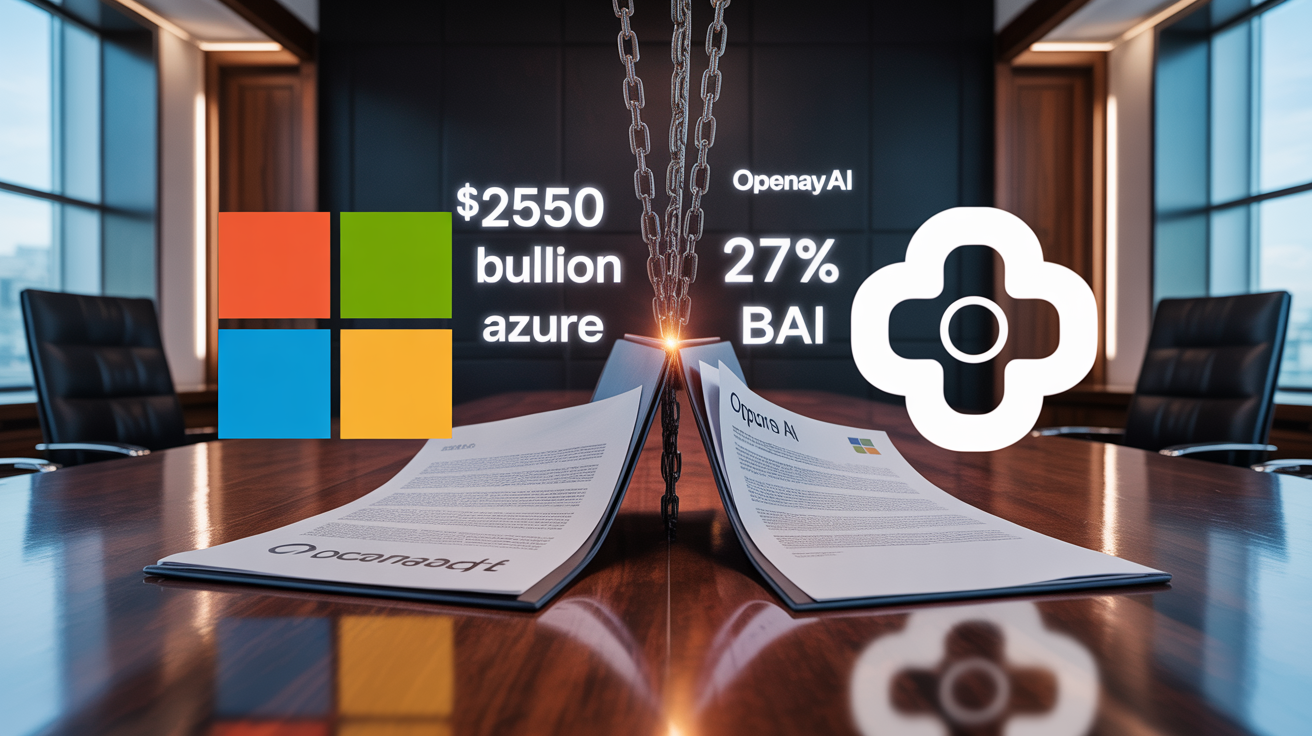

Microsoft's stake increased to 27% of OpenAI Group PBC (the newly restructured commercial entity), valued at approximately $135 billion. This represents the largest external ownership position in the company, with Microsoft's Board representation giving it significant influence over strategic decisions.

IP rights were extended through 2032—and crucially, now include post-AGI models. Previously, Microsoft's license to OpenAI's technology would terminate once the company achieved Artificial General Intelligence. Now, even after AGI, Microsoft retains rights to OpenAI's intellectual property for years to come.

A $250 billion Azure commitment locked in OpenAI's infrastructure spending with Microsoft through 2032. While the agreement technically allows OpenAI to use third-party cloud providers for some products, the API business—which generates the bulk of revenue—remains Azure-exclusive.

AGI declaration now requires independent verification. Previously, OpenAI could unilaterally declare it had achieved AGI, triggering the end of Microsoft's IP access. Now, an independent expert panel must verify any AGI claims, preventing OpenAI from using the AGI declaration as an escape hatch from its Microsoft obligations.

Microsoft can independently pursue AGI with third parties, eliminating OpenAI's de facto exclusivity in providing cutting-edge AI to its biggest partner and customer.

For OpenAI, this represents a golden cage. The company gains access to Microsoft's massive Azure infrastructure and continues receiving critical revenue share payments. But it loses flexibility, competitive positioning, and—most importantly—the ability to chart its own destiny.

"Microsoft has OpenAI exactly where it wants them," says a former executive at both companies who spoke anonymously. "Sam Altman talks about building AGI for the benefit of humanity, but the reality is he's built a company that can't function without Microsoft's permission. If OpenAI tries to leave or threatens Microsoft's interests, they can simply turn off the compute. Game over."

The October agreement also reveals Microsoft's long-term thinking. While OpenAI scrambles to compete with Google and Anthropic in the near term, Microsoft has secured rights to all of OpenAI's technology through 2032—including future models that might be developed years from now. Even if OpenAI becomes dominant again, Microsoft will be there to capture much of the value.

Some observers see parallels to Microsoft's relationship with Nokia in the smartphone era, or IBM's partnerships with countless software companies in the 1990s. In each case, a larger tech giant provided critical infrastructure and support to a smaller partner, gradually increasing dependence until the smaller company had no viable alternative.

"The question isn't whether Microsoft will eventually own OpenAI outright," says a Silicon Valley venture capitalist tracking the situation. "The question is what price Sam Altman will accept when he realizes he has no other choice."

Market Share Meltdown: Everyone Is Eating OpenAI's Lunch

While OpenAI battles Google and navigates its Microsoft relationship, a broader threat has emerged: it's losing market share to everyone simultaneously.

Anthropic's Enterprise Dominance

In July 2025, Menlo Ventures released a comprehensive survey of enterprise AI adoption. The results were stunning: Anthropic's Claude had captured 32% of the enterprise market compared to OpenAI's 25%—marking the first time OpenAI had lost the market leadership position in any category.

The gap was even wider in enterprise coding workloads, where Claude commanded 42% share versus OpenAI's 21%. For the high-margin enterprise customers that represent the future of AI monetization, Anthropic had become the clear preference.

In November 2025, Anthropic reinforced this lead with Claude Opus 4.5, a model that outperformed not just GPT-5.1 but also Google's Gemini 3 on software engineering benchmarks. On SWE-Bench Verified—a test of real-world coding ability using actual GitHub issues—Opus 4.5 achieved 80.9% accuracy versus GPT-5.1's 77.9%.

Perhaps more impressively, Opus 4.5 outperformed every human candidate in Anthropic's own two-hour engineering assessment, leading seven of eight programming languages on multilingual benchmarks. And it did so at dramatically lower prices: $5 per million input tokens and $25 per million output tokens, representing a 67% reduction from the previous Opus model.

The combination of superior performance and lower pricing proved irresistible to enterprise customers. According to reports from TechCrunch and Business Insider, Anthropic is in talks for new funding at a $350 billion valuation—nearly double its September 2024 valuation of $138 billion, and approaching three-quarters of OpenAI's $500 billion valuation despite having one-tenth the brand recognition.

DeepSeek's Open-Source Revolution

If Anthropic represents the premium alternative, DeepSeek represents the budget disruptor that could upend the entire industry.

Launched on January 20, 2025, by a Chinese AI startup, DeepSeek-R1 uses a mixture-of-experts architecture with 671 billion parameters (of which 37 billion are activated for each query) to achieve performance comparable to OpenAI's o1 model at 90-95% lower cost.

On key benchmarks, DeepSeek R1 either matches or exceeds OpenAI:

- AIME (mathematics): 52.5% versus o1 Preview's 44.6%

- MATH-500: 97.3% versus o1-1217's 96.4%

- Codeforces (competitive programming): 2,029 rating, beating 96.3% of humans

The real killer? Pricing. DeepSeek charges $0.55 per million input tokens and $2.19 per million output tokens. OpenAI's o1 costs $15 per million input tokens and $60 per million output tokens—roughly 30 times more expensive.

Even more disruptive: DeepSeek released the model under an MIT license, making it freely available for both academic and commercial use. Companies can download the model, run it on their own infrastructure, and never pay DeepSeek a dime.

Within days of launch, DeepSeek's mobile app topped both the iOS and Android app store charts, beating ChatGPT in downloads. Enterprise customers began evaluating whether they could achieve 90% of OpenAI's capabilities at 5% of the cost by switching to DeepSeek or fine-tuning it for their specific use cases.

"DeepSeek changes the entire economics of AI," explains a CTO at a Fortune 500 company who is piloting the technology. "Why would I pay OpenAI $1 million a month when I can get comparable results for $50,000 by running DeepSeek on my own servers? The math isn't even close."

xAI's Billion-Dollar Battle

Then there's xAI, Elon Musk's AI venture, which completed a $15 billion funding round in December 2025 at a $230 billion pre-money valuation. While the company's Grok chatbot is widely considered to lag behind Claude and GPT models in capabilities, xAI has made up for technical shortcomings with aggressive infrastructure investment.

The company's Colossus facility in Memphis now houses 200,000 GPUs, with plans for a 1 million GPU facility outside the city. An Atlanta data center added another $700 million in chips and networking equipment. xAI is seeking $3.5 billion in additional debt financing specifically for data center expansion.

Unlike OpenAI, xAI benefits from integration with Musk's other companies: X (formerly Twitter) provides training data and distribution, while Tesla offers a testing ground for real-world AI applications. In March 2025, xAI acquired X in an all-stock transaction that valued X at $33 billion and xAI at $80 billion—instantly giving Grok access to hundreds of millions of users.

The company also secured a $200 million Department of Defense contract in July 2025 for a government-specific version of Grok, demonstrating xAI's ability to win business that OpenAI has been unable to capture.

While Grok may not be the most capable AI model, xAI has proven that with enough capital, distribution, and integration with existing user bases, you don't need to be the best—you just need to be good enough.

The AI Bubble: A $3 Trillion Question Mark

Step back from OpenAI's specific troubles, and a larger question emerges: are we witnessing the early stages of an AI bubble collapse?

The warning signs are everywhere.

Big Tech companies spent approximately $400 billion on AI infrastructure in 2025 alone—Amazon, Google, Meta, and Microsoft combined. Hyperscalers accumulated $121 billion in debt over the past year, a 300% increase from typical borrowing patterns. Morgan Stanley estimates that $3 trillion in AI infrastructure spending will be needed through 2028, with only half covered by existing cash flows.

Stock market valuations have reached dot-com levels. The S&P 500 trades at 23 times forward earnings, while the Case-Shiller P/E ratio exceeds 40—a level not seen since the 2000 tech crash. And yet, actual revenue from AI remains a tiny fraction of the investment pouring in.

A November 2025 Bank of America survey found that 45% of investors now cite "AI bubble" as the number one tail risk for the economy and markets—a level of concern not seen since 2005, just before the financial crisis. The same survey revealed that a net 20% of fund managers believe companies are "overinvesting" in AI.

Even the CEOs building these systems admit there are problems. Sam Altman himself acknowledged in August 2025: "Are we in a phase where investors as a whole are overexcited about AI? My opinion is yes." Google CEO Sundar Pichai noted "elements of irrationality" in the AI market and conceded that "no company is going to be immune" if the bubble bursts.

The circular financing patterns raise additional red flags. Nvidia invests $100 billion in OpenAI, which then uses that capital to buy billions of dollars worth of Nvidia chips. OpenAI gives CoreWeave equity in exchange for data center capacity, then uses that equity to pay rent on the servers it's using. Each transaction creates the appearance of booming demand and validates the next round of investment, but it's not clear where the underlying economic value is actually being created.

Gary Smith, the Pomona College economist who has studied AI investment patterns, is blunt: "OpenAI is in a highly fragile situation and could be one of the first casualties if the AI bubble pops. When your business model is 'spend $2 for every $1 of revenue and hope that somehow becomes profitable in 2029,' you're not building a sustainable company—you're just betting that someone else will be dumb enough to keep funding you."

Ben Inker at GMO adds: "OpenAI's reliance on debt and very strange deals to fund its capital needs is deeply concerning given its significant losses. Nvidia's $100 billion investment raises serious questions about whether we're seeing genuine demand or just money flowing in circles to create the illusion of a market."

Perhaps the harshest assessment comes from Scott Galloway, who warns: "A financial collapse at OpenAI would trigger a systemic shock across global markets. They've created $1.15 trillion in commitments with no clear path to actually pay for them. When—not if—this unravels, there will be nowhere to hide for investors."

Not everyone agrees the sky is falling. BlackRock CEO Larry Fink argues that the "skyrocketing amount of capital" flowing into AI is a necessary investment for global leadership, not a bubble. Goldman Sachs analysts point out that tech companies are funding AI expansion with equity rather than debt, and that median cash flow for top US tech companies is triple what it was during the dot-com era.

But the fundamental question remains unanswered: when will AI actually generate returns that justify the trillions being invested?

What Happens Next: Three Scenarios

As OpenAI enters 2026, it faces a narrow path forward with three potential outcomes:

Scenario 1: The Miraculous Turnaround

In this scenario, OpenAI's engineering team delivers a breakthrough that decisively leaps ahead of Gemini 3 and Claude Opus 4.5. The new model—perhaps GPT-5.5 or 6—achieves dramatically lower inference costs through architectural innovations, making the economics suddenly viable. Enterprise customers return to OpenAI, attracted by the clearly superior technology. Revenue accelerates to $50 billion by 2027, $100 billion by 2029, putting the company on track to achieve the $200 billion needed for profitability by 2030.

Probability: 10-15%

The challenge is that OpenAI no longer has the technical lead it once enjoyed. Google and Anthropic have closed the gap, while open-source alternatives like DeepSeek are good enough for many use cases at a fraction of the cost. Achieving a decisive breakthrough would require not just incremental improvement, but a fundamental leap that hasn't materialized despite billions in R&D spending.

Scenario 2: The Slow Decline

OpenAI remains a significant player but gradually loses market share to better-capitalized rivals with superior distribution (Google) and better enterprise positioning (Anthropic). Revenue grows to $15-20 billion annually by 2027, but margins remain negative as inference costs and partner commitments continue to balloon. The company burns through multiple funding rounds, with each successive raise coming at worse terms.

By 2028-2029, OpenAI faces a choice: accept acquisition by Microsoft or another tech giant at a steep discount to its $500 billion valuation, or continue burning cash until the money runs out. Partners who borrowed billions to build infrastructure see their investments fail to generate expected returns, triggering a cascade of debt restructurings and asset sales.

Probability: 40-50%

This is the most likely outcome based on current trends. OpenAI isn't collapsing, but it's not winning either. The company becomes a cautionary tale about the difference between being first to market and building a sustainable business.

Scenario 3: The Catastrophic Collapse

The AI bubble bursts in 2026 or 2027, triggered by disappointing revenue growth, mounting losses, or a broader market correction. OpenAI's partners—Oracle, CoreWeave, SoftBank, and dozens of others—suddenly find themselves with tens of billions in debt backed by infrastructure that generates only a fraction of projected returns.

Defaults cascade through the system. Oracle's stock, already down $315 billion, loses another 50%. Bond markets freeze as investors reassess the risk of lending to companies with massive AI exposure. OpenAI itself, burning $8-10 billion annually with no path to profitability, announces it will wind down operations or accept a fire-sale acquisition by Microsoft at perhaps $50-100 billion—a 80-90% discount to its peak valuation.

The broader market impact is severe. Nvidia's stock crashes as its largest customers scale back orders. Cloud computing providers see massive write-downs on AI-specific infrastructure. Venture capital funds that loaded up on AI startups face a wave of portfolio company failures.

Probability: 25-35%

While this remains a minority scenario, the probability has increased substantially in recent months. The gap between AI investment and AI revenue continues to widen. Circular financing patterns make the system fragile to any shock. And OpenAI—sitting at the center of this web—is in an increasingly precarious financial position.

The Broader Lessons: What OpenAI's Crisis Teaches Us

Beyond the fate of one company, OpenAI's struggles illuminate broader truths about the current AI boom:

First, brand and first-mover advantage matter less than ever in technology. OpenAI essentially created the modern AI chatbot market with ChatGPT's November 2022 launch, building a brand recognized by hundreds of millions of users within months. Yet three years later, the company has lost market leadership in enterprises, faces competitive threats from multiple directions, and can't seem to turn technological innovation into sustainable profits.

Second, distribution remains king—especially for AI. Google's integration of Gemini across its entire ecosystem of 2 billion+ users represents an almost insurmountable competitive advantage. No matter how good ChatGPT becomes, it will never be pre-installed on Android phones, embedded in Gmail, or the default option in Google Search. OpenAI must convince every user to actively choose its product, while Google simply captures users by default.

Third, the economics of AI remain deeply uncertain. Despite billions in investment and years of development, no one has yet proven you can make money providing AI services at scale. OpenAI loses money on inference. Anthropic loses money on inference. Google and Microsoft can afford to lose money on inference because they have profitable core businesses, but even they can't sustain losses indefinitely.

Fourth, the infrastructure costs are staggering—and possibly unsustainable. The $1.15 trillion in commitments OpenAI has made, the $100 billion in debt its partners have accumulated, the millions of GPUs being installed in data centers worldwide—all of this is being built on the assumption that AI services will eventually generate returns that justify the investment. If that assumption proves wrong, the financial fallout will be measured in trillions of dollars.

Fifth, the AI race may be more about who can avoid losing than who can win. Google has search advertising revenue to fund its AI investments indefinitely. Microsoft has Office and Azure. Amazon has AWS and e-commerce. Anthropic has raised enough capital to operate for years without revenue pressure.

OpenAI? It has a $500 billion valuation based largely on potential, mounting losses, brutal competition, and a ticking clock counting down to when the money runs out.

The Bottom Line: The Emperor May Have No Clothes

Strip away the hype, the billion-dollar funding rounds, and Sam Altman's confident predictions of AGI, and OpenAI's situation is stark:

The company claims $20 billion in annualized revenue but appears to be generating closer to $6 billion in actual cash. It spends $8.65 billion on inference costs alone—before accounting for R&D, salaries, or any other expenses. It has committed to $1.15 trillion in infrastructure spending over the next decade without a clear path to paying for it. Its partners have accumulated nearly $100 billion in debt betting on OpenAI's success.

Meanwhile, Google's Gemini 3 is winning on benchmarks and user growth. Anthropic's Claude dominates the lucrative enterprise market. DeepSeek's open-source alternative costs 95% less. And even xAI, despite technical shortcomings, has more funding and better distribution.

The December "code red" memo wasn't a strategic pivot—it was a panic response to the realization that OpenAI's competitive position is eroding faster than its technology is improving. Cancelling expansion plans, refocusing on core products, and fast-tracking new models are the actions of a company in crisis, not one confident in its trajectory.

Can OpenAI turn it around? Certainly. The company still has world-class talent, substantial capital, and the ChatGPT brand. A major breakthrough is always possible. And the AI market is large enough that even a diminished OpenAI could be a billion-dollar business.

But the most likely outcome is that OpenAI becomes a cautionary tale about the difference between being first to market and building a sustainable business. The company that convinced the world AI was the future may not be around to see that future realized.

As Gary Smith warned: "OpenAI could be one of the first casualties if the AI bubble pops." Given the company's financial situation, competitive pressures, and unsustainable spending commitments, that prediction looks increasingly prescient.

The emperor valued at $500 billion may have no clothes after all. And in December 2025, everyone is finally starting to notice.

Sources & References

- 1. TechCrunch - "Leaked documents shed light into how much OpenAI pays Microsoft"

- 2. Forbes - "Sam Altman's 'code red' memo urges ChatGPT improvements as competition intensifies"

- 3. Menlo Ventures - "The State of AI in the Enterprise 2025"

- 4. Times of India - "OpenAI partners amass nearly $100 billion in debt"

- 5. CNBC - "Sam Altman warns investors may be 'overexcited' about AI"

- 6. Bank of America - "Global Fund Manager Survey"

- 7. Business Insider - "Anthropic's Claude Opus 4.5 debut signals new era of AI competition"

- 8. VentureBeat - "DeepSeek-R1 uses pure reinforcement learning to match OpenAI o1"

- 9. Morgan Stanley - "AI Infrastructure Investment Outlook 2025-2028"

- 10. Fortune - "OpenAI won't be cash flow positive until 2029 or 2030"

- 11. NPR - "AI bubble fears grow as investments soar past $400 billion"

- 12. Reuters - "Opinions split over whether we're in an AI bubble after billions invested"

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Markets and competitive dynamics can change rapidly in the technology sector. Taggart is not a licensed financial advisor and does not claim to provide professional financial guidance. Readers should conduct their own research and consult with qualified financial professionals before making investment decisions.

Taggart Buie

Writer, Analyst, and Researcher